The Battle of Gibraltar, 25 April 1607, by Cornelis Claesz van Wieringen – www.rijksmuseum.nl Image via Wikimedia

In the wake of the formal invoking of Article 50 by Prime Minister, no one knows with certainty the impact on the UK economy of leaving the European Union. Claims of imminent damage and possible disaster should be treated at best as informed speculation and at worst as more of the dysfunctional fear campaign that proved such ineffective argument for “remain”.

Much of the anxiety comes from the initial negotiating postures by the British government and the more vocal continental governments, magnified by the media’s proclivity to seize on the possibility of extreme outcomes. Among the more obviously diversionary are that the Spanish government might reassert claims to Gibraltar (taken seriously by the Guardian), and alleged British government hostility toward non-UK nationals (also hyped by the Guardian). In this anxiety-inducing context calls for calm are both rare and largely ignored (see for example, Larry Elliot’s discussion of trade outcomes).

As a result of the near-universal predictions of difficult negotiations leading to a severely negative economic impact of Brexit, criticism of the fiscal policy of the May government has almost disappeared from the media. In addition to the oft-asked question, what or how bad will be the effect of Brexit, attention in both Britain and on the continent should also address another query, is government fiscal policy helping or hurting?

Assessing fiscal policy begins with the obvious generalization that supply conditions set the constraint to economic growth in the long term, while in the short run the demand for goods and services determines the rate of economic expansion. When current production exceeds demand, the economy contracts or stagnates, and expands when demand depletes inventories, stimulating greater employment and output.

Brexit worries come from an anticipated fall in exports relatively to imports due to loss of EU trade advantages, plus a possible decline in private investment caused by reduced business optimism. The third component of private demand, consumption expenditure, would tend to move with the other two, since exports and investments are the major drivers of household income.

Economies have a fourth source of demand, public expenditure. Brexit commentary has treated public sector effects as negative because of an anticipated revenue short fall derivative from lower growth, using a favourite but inappropriate “black hole” metaphor (cosmic black holes are not empty spaces, quite the contrary, they are unimaginable dense). This emphasis on revenue effects reflects the almost universal endorsement by the media of the balanced budget ideology, that a fiscal deficit is ipso facto a serious problem.

If we go beyond the dubious economics of balanced budgets, we can ask a constructive question – how might fiscal policy contribute to stabilizing the UK economy should Brexit effects prove substantially negative? The question has an obvious answer and it is not ex-chancellor Osborne’s roof mending on sunny days (i.e. generating a budget surplus). Should exports fall or investment decline, or both, a counter-balancing fiscal expansion would be the appropriate action. As a transitional measure, public expenditure replaces private.

Behaviour of the two Conservative chancellors since May 2010 suggests that using fiscal policy to aid the stabilization of the economy is beyond their conceptual grasp, as it appears to be among the eurozone finance ministers (“Eurogroup”). Even before the 23 June referendum, Jeremy Smith among others argued that fears of a “Brexit slowdown” function to obscure the much more obvious drag on the UK economy, fiscal austerity.

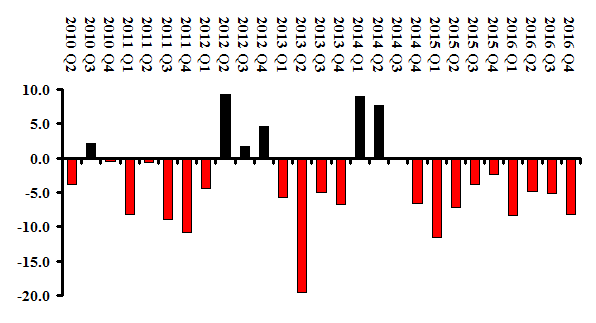

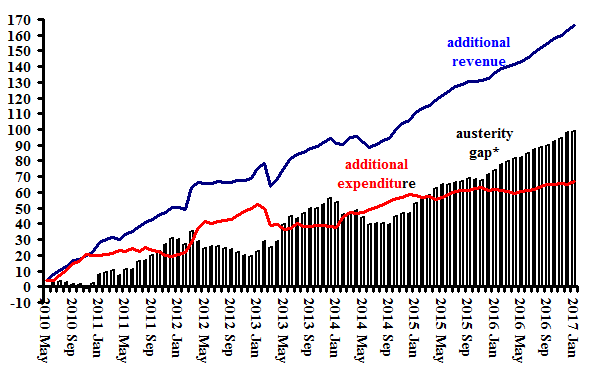

The numbers overwhelmingly support Smith’s “austerity slowdown” hypothesis, as the chart below demonstrates. The vertical axis measures the growth in central government revenue and expenditure since May 2010 when Chancellor George Osborne’s austerity ideology became policy. By January 2017 pubic revenue had increased by £166 billion, compared to £67 billion for expenditure.

These numbers imply that over almost seven years Conservative chancellors took a net £100 billion out of the economy, an extraction I label as “fiscal drag”. Far from fostering a stronger and more stable economy, Mr Osborne weakened it, relying with little success on private demand not only to recover its own momentum after the Great Recession of 2008, but to cover public sector’s drag as well.

Austerity Drag: Revenue and Expenditure Growth since April 2010

*Change in revenue minus change in expenditure.

Source: Office of National Statistics.