From the March 2016 Preface to The Economic Consequences of Mr Osborne

By Professor Victoria Chick, Ann Pettifor and Geoff Tily

… when sustained, fiscal consolidation increases rather than reduces the public debt ratio and is in general associated with adverse macroeconomic conditions. ‘Economic Consequences of Mr Osborne’, June 2010

Having missed the genuine threat of the private debt bubble, the economics profession misread disastrously the increase in public debt. In their 2009 This Time is Different, Kenneth Rogoff and Carmen Reinhart discreetly warned:

However, the surge in government debt following a crisis is an important factor to weigh when considering how far governments should be willing to go to offset the adverse consequences of the crisis on economic activity. (290)

Shortly afterward their paper ‘Growth in the Time of Debt’ set an explicit threshold of 90 per cent of GDP above which adverse economic conditions became statistically significant. In the UK, academic, City and media economists warned politicians in no uncertain terms that it was imperative to reduce the public debt. On 14 February 2010, 20 of the most senior UK economists (listed below) wrote to The Sunday Times castigating the Labour government for inadequate efforts on deficit reduction and setting the tone not only for the general election of that year but seemingly ever since.

Orazio Attanasio, UCL; Tim Besley, LSE; Roger Bootle, Capital Economics; Sir Howard Davies, LSE; Lord (Meghnad) Desai, House of Lords; Charles Goodhart, LSE; Albert Marcet, LSE; Costas Meghir, UCL; John Muellbauer, Nuffield College, Oxford; David Newbery, Cambridge University; Hashem Pesaran, Cambridge University; Christopher Pissarides, LSE; Danny Quah, LSE; Ken Rogoff, Harvard University; Bridget Rosewell, GLA and Volterra Consulting; Thomas Sargent, New York University; Anne Sibert, Birkbeck College, University of London; Lord (Andrew) Turnbull, House of Lords; Sir John Vickers, Oxford University; Michael Wickens, University of York and Cardiff Business School.

In June 2010, the Coalition government took office, and George Osborne announced fiscal consolidation plans to meet the concerns of Labour’s critics.

The analysis in the ‘Economic Consequences of Mr Osborne’ – published in July 2010 – was prepared as a reaction to this latest manifestation of academic influence over political consensus. We sought to learn from the record of history embodied in the National Accounts. As the quotation at the head of this paper shows, we were careful not to claim too much.

Some six years later, vast damage has been inflicted on public services and the public sector workforce. Five years of consolidation became ten years, with total spending cuts virtually doubling in size. The economy has barely expanded in per capita terms relative to the pre-crisis peak, and public sector debt as a share of GDP is still rising in spite of a vast fire sale of public assets.

Our analysis showed it would have been unwise to expect anything else.

Various authors objected to our technique as lacking in scientific or econometric rigour, or as simply self-fulfilling on account of the relation between debt and the deficit and between government expenditure and income. Given these relations between variables and their non-homogeneity over time, no technique, simple or complex, is infallible. The best technique we maintain is to study the results of economic policy as distinct episodes from history that might advise present actions, not as variables in a regression.

The acclaimed contributions to the austerity case were far more culpable of methodological error; our particular bugbear was the (still) commonplace usage of the deficit as a guide to the extent of austerity. Alesina and Ardagna’s work on which the Treasury case rested heavily, had already been dismantled (see page 33, n.29). Now Rogoff and Reinhart have been discredited in a very public way. With the evidence thin on the ground in the first place, there is very little reputable evidence left for the beneficial effects of austerity. Conversely, more and more evidence has accumulated against austerity.

International organisations have been responsible for much of this evidence. First the IMF revised their previous estimates of multipliers to substantially higher figures, which they say better reflects recent evidence. The OECD has also moved towards a more expansionary stance, culminating in their 18 February 2016 interim Economic Outlook. The press release includes this categorical re-assertion the Keynes position, no truer now than it was five or eighty-five years ago:

A commitment to raising public investment collectively would boost demand while remaining on a fiscally sustainable path. Investment spending has a high multiplier, while quality infrastructure projects would help to support future growth, making up for the shortfall in investment following the cuts imposed across advanced countries in recent years. These effects would be enhanced by, indeed need to be undertaken in conjunction with, structural reforms that would allow the private sector to benefit from the additional infrastructure; notably in the Europe Union, cross-border regulatory barriers are a significant obstacle. Collective public investment action combined with structural reforms would lead to a stronger GDP gain, thereby reducing the debt-to-GDP ratio in the near term.

Commentators in the UK press have also recanted, even The Economist. The following comes from the editorial in the issue of 20 February, 2016:

…governments can make use of a less risky tool: fiscal policy. Too many countries with room to borrow more, notably Germany, have held back. Such Swabian frugality is deeply harmful. Borrowing has never been cheaper. Yields on more than $7 trillion of government bonds worldwide are now negative. Bond markets and ratings agencies will look more kindly on the increase in public debt if there are fresh and productive assets on the other side of the balance-sheet. Above all, such assets should involve infrastructure. The case for locking in long-term funding to finance a multi-year programme to rebuild and improve tatty public roads and buildings has never been more powerful.

In 2012, when austerity in Britain was really hurting, the New Statesman, under the headline ‘Osborne’s supporters turn on him – leading economists who formerly backed Osborne urge him to change course’, reported going back to TheSunday Times’s 20 economists to ask whether they now stood by what they had written. Only one of the twenty still did so unreservedly. Extracts from specific responses are reproduced in the annex, at the end of this preface (p.11). None admit to an error of judgement; all plead changed circumstance (we return to this below).

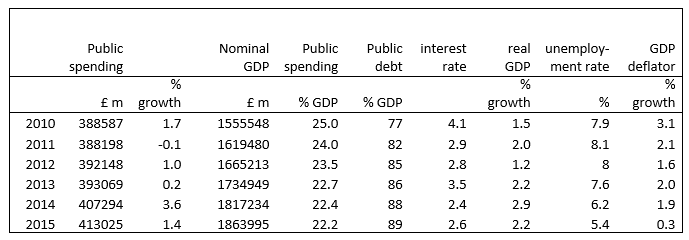

The UK was spared the worst ills of austerity when, late in 2012, policy was relaxed rather than intensified as the original doctrine of The Sunday Times’s 20 economists would have required. Moreover (without belittling the undoubted hardship caused) from a macroeconomic perspective the policy was already relatively moderate by the standards of historical experience, amounting basically to a sharp reduction in the rate of growth of nominal expenditure. (NB we used general government final consumption and investment expenditures as the indicator of discretionary contraction.) Under the original plan, government expenditure was to be virtually flat, averagingan increase of 0.075 per cent a year; after the relaxation, spending was expanded by 1.2 per cent a year (measured over 2010 to 2015; as a guide to the scale of the reduction, in the six years before the coalition spending grew by 6.5 per cent a year). The figures for these years, across the same categories as the tables in the main paper, appear below. (These are on the latest national accounts definitions and so do not continuously follow from Table 3I.1 in the main text. The main charts are updated in the annex to this preface on p.14).

As expected, economic growth was reduced significantly, averaging 2.0 per cent a year over 2010 to 2015 compared with 2.6 per cent a year over 1948 to 2007. (In fact, the recovery was the slowest over the whole period for which UK figures are readily available, even slower when measured per head and even more abrupt in nominal terms). Slower economic growth meant lower growth in labour income and profits and therefore lower than expected government revenues and increased welfare expenditure. Like everybody else we missed the strength of the employment response, but the parallel unprecedented reduction in earnings growth amounted to the same thing in terms of tax revenues, and welfare payments were higher because of in-work benefits (housing benefit and tax credits).

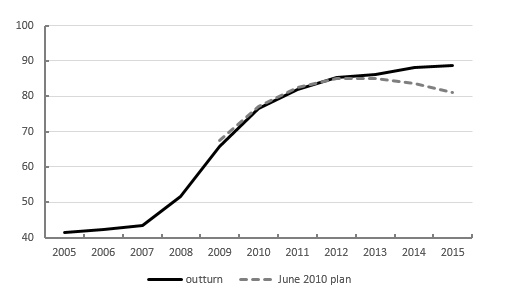

As a result of this shortfall in net receipts, the deficit was reduced by much less than expected by the coalition. On the basis of what happened to the public debt ratio, our conclusions have been wholly vindicated. While stock/flow debt/deficit relations mean debt would inevitably rise relative to 2010, according to the original plans it should by now have been on an improving trajectory. Figure A shows outturn against plan on the basis of the Maastricht definition that was used in the original work. Rather than improving, the debt ratio has not stopped rising and in 2015 was within a whisker of 90 per cent of GDP. The difference between the plan and outturn is 7.5 percentage points of GDP, i.e. £140 billion.

Figure A: Public debt as a percentage share of GDP