“The state has no source of money, other than the money people earn themselves. If the state wishes to spend more it can only do so by borrowing your savings, or by taxing you more. And it’s no good thinking that someone else will pay. That someone else is you.”

“There is no such thing as public money. There is only taxpayers’ money.”

Mrs Thatcher, speech to Conservative Party Conference, October, 1983.

“We know that there is no such thing as public money – there is only taxpayers’ money”

David Cameron, on the campaign trail, 6 April, 2015.

Quantitative Easing: ‘new money that the Bank creates electronically’.

Bank of England website in ‘Quantitative Easing: how it works.’[ii]

“When a bank makes a loan to one of its customers it simply credits the customer’s account with a higher deposit balance. At that instant, new money is created.”

Bank of England Money in the Modern Economy: Quarterly Bulletin, Q1, January, 2014.

Introduction

At the heart of the politically inept responses to the 2007-9 Great Recession is an ideologically-driven and mendacious conviction: that while society can afford to bail out a systemically broken banking system, Trident and the HS2 railway extension, it cannot afford to finance the NHS, higher education, skilled apprenticeships, an expansion of broadband and the arts.

The “there is no money’ mantra suggests that governments and their central banks do not have the powers to address economic failure, youth unemployment, energy insecurity, climate change, poverty and disease. The only money available for these activities, allege some politicians, is taxpayers’ money. These same politicians do not explain how first £375bn was found to bail out the banks; and then an additional £55bn was raised (‘out of thin air’) by the Bank of England to subsidise banks through the government-initiated Funding for Lending scheme. [iii]

We disagree with the ‘there is no money’ mantra. Within a sound financial and monetary system, there need never be a shortage of money to meet society’s needs. There may be limited resources, and limited brainpower but there need never be a shortage of money. In this briefing I set out to explain why.

Mrs Thatcher, whose microeconomic views on the economy still inform the policies of most of our political parties, gave clearest expression to the wrong and economically flawed notion that ‘there is no money’ – in the 1983 speech cited above. David Cameron repeated that speech verbatim thirty two years later, on Monday 6th April, 2015 as part of the campaign to secure his re-election as prime minister. “We know that there is no such thing as public money – there is only taxpayers’ money” he is reported to have said, without crediting Mrs Thatcher. [iv]

Today this assertion by both Conservative Prime Ministers sits strangely with the facts of the recent bailout of the global banking system, when the Bank of England created first, £375 billion as part of the bank bailout; and then issued another £55 billion as part of the Funding for Lending scheme. It also sits strangely with a private banking system that ‘prints’ 95% of Britain’s money supply (by creating money ‘out of thin air’), and uses some of that money to finance government debt.

While politicians try to persuade electorates that ‘there is no money’ something quite different happened under the guise of ‘Quantitative Easing’. Central bankers around the world created trillions of dollars ‘out of thin air’, and did so ‘overnight’ to bail out the global banking system. The Governor of the Bank of England explained to a Scottish conference in October, 2009 that

a trillion (that is, one thousand billion) pounds, close to two-thirds of the annual output of the entire (British) economy”[v]

had been mobilised (again, almost overnight) to bail out the British banking system.

Never in the field of financial endeavour … has so much money been owed by so few to so many.[vi]

Despite this evidence that the state does indeed have “other sources of money” – other that is, than taxation – many have adopted Mrs Thatcher’s reasoning.

Dear Chief Secretary, I’m afraid to tell you there’s no money left,

wrote Liam Byrne, a British Labour Treasury Minister, in a letter to his successor and published in the Guardian, on 17th May, 2010.[vii]

The British government has run out of money because all the money was spent in the good years …

said George Osborne, Britain’s Chancellor of the Exchequer on Sky News on the 27th February, 2012.

We will have to govern with much less money around.[viii]

noted Ed Balls, Britain’s opposition Chancellor, in a speech: Striking the right balance for the British economy, delivered at Thomson Reuters, on Monday 3rd June, 2013.[ix]

Where does money come from?

All money begins life as a promise, or credit (based on the Latin word ‘credo’ I believe): “I promise to pay the bearer…” Promises to repay are underpinned by a system of powerful institutions: the law of contract, the criminal justice system, the system of accountancy, and the monetary system. These help to uphold all promises, or credit, made through the banking system. When the money created ‘out of thin air’ by the commercial banking system enters the economy, it can have both a reinvigorating impact on economic activity, but also a deleterious impact. It can on the one hand lead to increased investment, the creation of jobs, the generation of income and the repayment of debts. Alternatively too much money in an economy already at full employment and full capacity, can lead to the inflation of asset prices, wages and consumer prices. New money directed at speculation and other forms of gambling – in property, commodity prices and other financial products, can inflate the prices of those assets and goods and lead to increased financial volatility and crisis.

So the monetary system must always be managed, to ensure new money is used productively, and to maintain wider economic stability.

Almost all new money (95% in the UK and 99% in the US) is created by commercial banks when they extend or create credit. While the central bank plays a critical role in managing the financial system, the Bank of England only creates 5% of the UK’s money supply. The money supply is created by private solvent commercial banks, and it expands each time a borrower (like you or me) applies for credit. (If we (as a whole) fail to apply for credit, the money supply contracts.) Only when the banking system fails, as in 2007-9, does the central bank step in an attempt to expand the money supply.

Credit creates deposits, and not the other way around, as the Bank of England confirmed in 2014, in the quotation cited at the beginning of this article.

In other words, textbooks (and politicians) are wrong when they suggest that taxpayers’ money has to be raised to finance expenditure; that deposits or savings must be used to create loans; or that we need first to raid piggy banks, or accumulate savings, in order for banks to lend, or to finance public and private projects.

Instead the Bank of England explains that the reverse happens: loans are used to create deposits, or finance, or savings. And all licensed, commercial banks (as opposed to savings banks) can create deposits or savings. That is, provided they are not insolvent and there is demand from borrowers – applying for new loans or mortgages.

These loans are subject of course to the availability and value of the borrower’s collateral (e.g. property); and to the signing of a contract or promise to repay over a fixed term at a certain rate of interest.

While commercial banks can create any amount of money through lending, only central banks can create legal tender – tangible money (notes and coins, or cash). However, tangible money today forms a very small part of all the digital money used on a daily basis, and of total liquidity. Only tiny amounts of money are ‘printed’ or minted. Since the foundation of the monetary system in 1694, most money has been and is created simply by entering numbers into a ledger (‘fountain pen money’) or into a computer – and then transferring it to the borrower’s account.

That is the wonder of a well-managed monetary system.

The central bank also takes responsibility for what is known as ‘base money’ – the money that underpins, in Britain’s case, the value of the UK’s currency, sterling. That is an altogether more complicated story, which will not be dealt with here.

Quantitative Easing is not taxpayers’ money

During the crisis, and because of the failure of the private banking system, central bank monetary operations took on great significance, and came to be known as ‘Quantitative Easing’ or QE. In Britain the nationalized Bank of England launched QE to help expand Britain’s money supply. It was forced to do so because the money supply and the private banking system had contracted and crashed as a result of banking fraud, incompetence and the resulting generalized financial crisis.

As part of QE operations central banks inject large amounts of electronically created ‘money’ or ‘liquidity’ into the private financial system. They do so as part of their routine monetary operations, intended to maintain financial stability, to encourage bank lending and to influence rates of interest. There is nothing new about this: central banks have undertaken this role for about three hundred years now.

This expansion of the money supply is achieved by the following means. The Bank creates ‘money’ electronically and provides it to banks in exchange for assets (including government bonds or IOUs) owned by participating banks.

Central banks can only create liquidity and expand the money supply as part of a process that involves pre-existing bonds or debt. Just as credit is important to kick-start economic activity, so bonds, or public and private debt are central to the process of creating new money, or liquidity. Well managed debt is also important as an asset for safeguarding the future value of financial assets e.g. pensions.

Private banks or financial institutions have accounts with central banks, like the Bank of England. These private banks purchase and hold sovereign (i.e. government) and corporate bonds, issued by the treasury departments of both governments and firms. Central banks undertake the liquidity or money-creating role in concert with private financial institutions. They do this by exchanging government or corporate bonds owned by private financial firms for central bank ‘reserves’ -which provide liquidity or new ‘money’.

So government bond issuance or debt, is both a way of expanding the money supply, and of raising public finance. This finance can be raised without recourse to taxpayers. That is why politicians mislead the public when they argue “there is only taxpayers’ money”.

The bonds purchased by central banks for the purpose of creating liquidity (‘reserves’), are most often AAA-grade bonds (debt) issued by governments and big corporations (and due for repayment over different periods of time and at different rates of interest).

If governments are say, committed to austerity policies and do not issue new bonds or debt (for the purpose of investment) then a shortage of bonds in the capital markets can constrain the central bank’s ability to expand reserves, and with it the money supply. A shortage of such AAA-graded debt can cause distortions in the economy.

We see this most clearly in the case of Germany today, where the government’s net investment in the economy is negative. Public infrastructure is decaying, and economic activity waning. This is one side effect of the lack of public borrowing and investment, but there is another. Pension funds and other investors face a shortage of German AAA-graded assets to purchase as an investment in the future. The third side-effect of the German government’s ‘frugality’ is that the European Central Bank (ECB) is constrained in its ability to create new money by the shortage for exchange purposes, of those very same AAA-rated German government bonds.

Can QE fix the economy?

Central bank reserves created as a result of QE operations are not ‘savings’ and they are not a form of money that can be ‘lent on’. Instead QE is a form of finance directed exclusively at approved institutions that operate in secondary financial markets.

For these banks or institutions central bank reserves are simply a type of ‘overdraft’. They are used to manage, simplify and balance the daily ‘clearing’ system between banks. A commercial bank’s ‘overdraft’ with the central bank has a ‘limit’ – depending on the size and creditworthiness of the bank. This ‘limit’ can be secured (or not) against collateral.

This ‘limit’ (known as central bank ‘reserves’) is not money or a deposit, but like all overdrafts, it does expand the commercial bank’s purchasing power.

By exchanging assets (for example bonds or mortgages) for central bank reserves, the commercial bank increases its overdraft ‘limit’ with the central bank. We repeat: the ‘limit’ itself is not money. But reserves free up the balance sheet of the private bank, and enable it to, in turn, pay the original owner (e.g. a pension fund) for the purchase of a bond with money that it has obtained as a result of the exchange of that bond with the central bank.

After expanding its reserves, the commercial bank is able to make the payment to the pension fund by entering a number into its computer, and transferring a sum into the pension fund’s account. The reserves are not lent on. They stay inside the banking system.

The impact of QE on asset prices, and on the economy

By taking bonds and other swapped assets on to its balance sheet, the central bank removes those assets from the market place, which leads to a shortfall, and therefore causes the price of the bonds to rise. When bond prices rise, their yield (the return that investors can expect to make from the bond) falls. Because government bond yields influence all other interest rates, the central bank’s QE purchases are intended to do just this: cause interest rates to fall across the board.

In this endeavour both the Bank of England and the US’s Federal Reserve succeeded after the financial crisis of 2007-9. Interest rates fell, and have remained relatively low since the launch of QE. (This is not true for all rates on loans, but it is true for the central bank lending rate (the ‘base rate’) which has had some impact on other rates, including mortgage rates.)

Right now, in March 2015 this process is happening across the Eurozone, interest rates are falling across the zone, in expectation of the ECB’s purchase of sovereign bonds, via QE. Indeed as noted above, rates on German government bonds are negative. In other words, lenders are paying the German government for lending the money – a bizarre anomaly.

Lowering or raising interest rates is the most important aspect of central bank monetary operations. These operations are a vitally important function of monetary policy, as interest rates have a deeper and wider impact on the economy as a whole.

QE also provides additional resources (via the commercial banking system) to those relatively select few institutions and individuals that own government and corporate bonds. Regrettably QE does not have the effect of forcing banks to lend into the real economy. The Bank of England does not have the power to coerce banks into lending. Instead commercial banks have taken the resources provided by QE and used these to clean up their balance sheets, where liabilities exceed assets. Bank lending in the UK has been negative for most of the years since the crisis, and remained so after the launch of the Bank of England’s QE programme. In other words, QE has failed to transmit money into the real economy. Instead both company, SME and individual savers have deposited more in banks, than banks have made available in new loans to corporates and SMEs.[x]

Swapping assets like bonds for central bank-created liquidity has also not encouraged the rich owners of those bonds to invest, or to spend that money. And if owners (e.g. pension funds) of swapped assets lack confidence in the health of the economy, then no amount of QE will stop their hoarding of these assets, and encourage further investing.

So while QE may have saved the banking system from collapse, it has not helped revive wider economic activity. Nor is it mandated to do so. QE is aimed at stabilizing just one part of the economy – the financial sector, and at lowering rates for the economy as a whole. It is not aimed at expanding the wider economy. In the event of a slump in private investment, only public investment can expand employment and economic activity.

QE does not create demand in a slump caused by the failure of the private financial sector. Only government investment can create demand.

QE, inflation and benefits to the wealthy

While QE can and does inflate the value of assets (government bonds, equities, property) bought and sold in secondary markets, it is not, as argued above, aimed at the economy as a whole, and therefore does not cause price or wage inflation.

In this sense QE favours the wealthy, by inflating the value of their assets, while not affecting the prices of goods they buy, or the wages of people they employ. Indeed both prices and wages have fallen dramatically since 2008. [xi]

Central bank resources helped bail out reckless and often fraudulent private bankers and others in the finance sector. Financial traders, hedge funds, investors, bankers, wealthy individuals, property-owners and speculators benefited from the Bank of England’s QE, as the Bank itself admitted. But then so did pension funds – in which large numbers of people have a stake.

They benefitted because they are lucky, or skillful or big enough to own such assets. The poor, and a large swathe of the middle classes, tend not to own assets, and instead live not from rent earned on assets, but from wages, salaries or pensions. According to the Bank of England “the median household held only around £1,500 of gross assets, while the top 5% of households held an average of £175,000 of gross assets.” [xii] The Bank went on to calculate that the value of shares and bonds had been inflated by QE by 26% – or £600bn – equivalent to £10,000 for each household in the UK. 40% of the gains went to the richest households.

While private investors will have made gains from QE, the weakness of the wider economy means that most lack the confidence, or incentives, to risk further investment. This is because the private sector is still heavily indebted; both the UK and the global economy are still unbalanced and volatile, and deflation looms.

The Bank of England’s QE resources did not, and cannot, reach or benefit the asset-poor; and did not, and cannot stimulate wider economic expansion. To repeat: this is because the purpose of QE is to influence monetary policy, and it does so via the financial sector and wealthy pension fund and corporate owners of assets.

Only government investment and government spending can benefit the whole of society because of its wider impact on the economy.

How QE impacted on the rest of the economy

However, because the private banking system was on the brink of collapsing, central bank resources did help to stabilize the financial system – a process from which we all benefited. (There was a moment during the crisis apparently, when the threat that ATMs would be closed down was real. We’d have all lost money if that had happened.) QE also helped protect the assets of pension funds, and lowered interest rates. Lower rates reduced private sector debt repayments, as those with debt and especially mortgages quickly discovered.

However, while QE may have lowered rates of interest, this has not helped the economy much as the problem (at this moment in time) is not interest rates, but the sluggish, over-indebted, depressed and unbalanced economy. There is a lack of demand for goods and services – even while there is an urgent need for, for example, medical care, alternative and sustainable energy, greater energy efficiency, decent housing, expanded broadband access, skills training and low-carbon transport.

Only the public sector, in the event of a slump in private investment, can fund and expand investment in these sectors – particularly in the new, and still ‘risky’ areas of the green economy. By doing so, only government can give confidence to, and stimulate the private sector into investing in, for example, the transformation of the economy away from a dependence on carbon.

Below we discuss how government investment can be funded – without direct recourse to taxpayers.

Can the Bank of England support government spending?

Britain is a signatory to Article 123 of the European Union’s Lisbon Treaty (agreed in 2007 by the Blair government and ratified in 2009 by Gordon Brown as Prime Minister). Under this Article the government is forbidden from directly using the Bank of England’s resources to finance government spending. But as Frances Coppola has argued,[xiii] Article 123 is redundant because, as we show above, monetary financing of government expenditures is provided by private, commercial banks, pension funds and other institutions (when they purchase government bonds in the bond market). Central banks always “passively support that financing” by supporting the private commercial banking system – through routine monetary operations that have come to be known as QE.

Can the Bank of England bypass the moribund banks and purchase assets like land, directly?

Professor Richard E. Werner has proposed[xiv] that central banks should simply bypass the private banking system, and purchase a range of different assets, directly. In 1994 he suggested that the Bank of Japan should purchase land in Tokyo, and turn it into parks, thus enhancing the environment, reviving the property market and boosting the banking system.

However, if the central bank, and in particular the Bank of England were to undertake purchases of land, it would quickly become politicized. The Bank would be using its extraordinary powers (backed by taxpayers) not to manage and stabilize the monetary system, but to intervene in the economy.

Imagine the uproar if the Bank of England were to resolve to use its great powers to compulsorily purchase land in London? It is challenging enough for elected governments to undertake the compulsory purchase of land for the purposes of expanding for example, the (HS2) rail network. But elected governments enjoy an electoral mandate. The board of the Bank of England is not made up of elected representatives. Instead it is made up of technocrats and financial experts, many with close links to the private financial system. They would be bypassing an elected government, and using what would quickly and correctly be defined as fiscal (i.e. taxpayer-backed) resources, to intervene in the property market.

Prof. Werner’s proposal should instead be directed at government departments governed by elected politicians and whose remits include for example, the purchase of land and the maintenance of public parks. In a depressed property market, the purchase of land by government for the purpose of enhancing the environment, and stimulating the economy might well prove acceptable to the electorate. However, there is no need for this process to be undertaken by the central bank, which has a narrow, monetary mandate, and an unrepresentative and unaccountable board.

Is government-funded ‘helicopter money’ an option?

The government could provide direct financing to individuals and households, and could do so in the form of tax rebates. The Labour government under Gordon Brown achieved this after the crisis broke, by cutting VAT. The US administration, as part of its 2008 economic stimulus package distributed tax rebates worth $100bn to US citizens in 2008. By the 1st July, 2008, more than seventy million American households had received tax rebates of about $950. [xv]

In October 2008, Australia’s Labour government, led by Kevin Rudd, implemented a stimulus package which disbursed a Christmas bonus to low and middle income families. They received $1000 per child; single pensioners received a $1400 payment and pensioner couples $2100 under an emergency $10.4 billion rescue package announced “to protect the economy.”

These packages were funded initially by government borrowing (through the issuance of government bonds) and were passively supported by the Bank of England, Federal Reserve and the Australian Reserve Bank.

Could the Bank of England disburse ‘helicopter money’?

While central banks are prohibited from financing government spending, the Bank of England could simply bypass the government and distribute funds (perhaps £6,000 each – equivalent to the £375bn of QE) to all individuals on the electoral register, as John Muellbauer has suggested. [xvi] Such an action, he suggests, would be proof of a central bank’s independence from government. And the “multiplier’ effect would mean that additional tax revenue from this disbursal of funds for spending by individuals, would improve the government’s finances.

What are the drawbacks to ‘helicopter money’?

The problem with the central bank or government dropping wads of money on British households is that the money would probably be used for consumption, not investment. Households would go shopping for goods and services, and because Britain is such an open economy, and manufactures form a small part of output, most of the money for goods would leak to, for example, China.

That would not necessarily increase employment in the UK, and would further imbalance our economy which already has a large and unsustainable trade deficit.

And in any case, excessive consumption invariably leads to an increase in greenhouse gas emissions, as more ‘stuff’ is made from the earth’s finite assets, and transported around the global economy.

The alternative?

Far preferable would be a programme of public investment in productive, labour-intensive, and sustainable ‘green’ infrastructure – leading to for example, greater energy efficiency, and the substitution of clean energy for carbon. Such infrastructure investment would create employment here in the UK, and would make much greater use of local resources. Above all it would generate income – in the form of profits, wages, salaries and tax revenues.

That is what the Green New Deal group proposed way back in July, 2008: a £50 billion programme of green infrastructure investment. This is no more than the proposed expenditure of £50bn on HS2 – the high speed rail network.

It is unlikely that £50 billion would be spent in just one year, as it takes time to prepare for, disburse and implement big investment projects. So the government would only need to raise a proportion of the total every year for several years.

It would do so by progressively issuing bonds, to suit different purposes.

These bonds would be issued over different time periods (1 year to 50 or even 100 years) and at different rates of interest. Some could even be ‘hypothecated’ – designated as intended for specific purposes. ‘Green bonds’ aimed at particular infrastructure projects could become as popular with individuals and institutions as Harold Macmillan’s Premium Bonds (issued in 1956) once were.

Professor Weeks has argued that if “we accept the argument made by many that governments should operate more like households and businesses then governments should borrow to invest. At the present moment this option is especially relevant because the UK government holds ownership in two major private banks, RBS and Lloyds.” The government is in a position to demand from these banks, extremely reasonable rates and terms of repayment on its bonds.

The taxpayer-backed stakes in these two major banks gives government leverage over these commercial institutions. As such, the government could require RBS and Lloyds to finance the Green New Deal as one of the ‘terms and conditions’ for the bank bailout; for government guarantees and for the nationalized Bank of England’s very, very low rates of interest for banks. The “conditions” could include the purchase of government “Green bonds” at very, very low rates of interest, repayable over many years. This is what the commercial banks were required to do during World War II – to help finance the war effort.

Where would the £50bn to finance the Green New Deal come from?

The straightforward answer is: from borrowing, or bond issuance, which as indicated above, is an important part of a functioning monetary system.

Just as businessmen and women invest in updating their firm’s equipment and skills, with a view to expanding the business; and just as homeowners borrow long-term to gain a secure home, and then invest in its improvement, so government must borrow to invest in the long-term improvement of the nation’s skills, equipment and infrastructure.

Thanks to the Bank of England’s QE programme, both public and private investors in green infrastructure projects can now borrow from banks or financial institutions at very low rates of interest. Indeed government borrowing rates today are probably the lowest on record. If the government were to take out a 30-year ‘mortgage’ today – it would lock in an extraordinary low rate of interest, for the next thirty, fifty or one hundred years. Contrary to scare stories put about by the media, this investment could create skilled, well-paid jobs. This expanded level of employment would generate more in income and tax revenues (via corporation tax, PAYE & VAT) than the low cost of repayment on bonds, and would therefore, represent a very light burden for future taxpayers – who would anyway enjoy the long-term benefits of that investment. At the same time, because the government can rely on tax revenues, such debt represents a very safe bet for bond buyers, in particular pension funds wanting to secure future pension payments.

Indeed it is crazy for the government not to borrow on these terms, and use the opportunity for example, to transform our economy away from toxic carbon, or to expand access to broadband, educate and skill up the young, and expand the arts.

Its crazy because by borrowing to invest in sound, labour-intensive infrastructure projects, the government will begin to generate income: private income for the contractors and employees that benefit from the investment, as well as public income in the form of tax revenues. And future tax revenues paid by those whose employment is the result of public investment, should easily cover the cost of the very low interest, long-term bond issues used to finance the investment.

For example: a government scheme to improve public transport would likely engage a large number of private construction or transport companies, as well as public sector employees. These private companies would make a profit on their work for government, profits that will be taxed, sending money straight back to the government’s coffers, to help pay down the debt. By employing skilled, well-paid staff to fulfill a public contract, a private company would create income for those employees. Not just private income in the form of wages and salaries, but both PAYE and VAT tax revenues for the government too.

At the same time, the government would be saving on social welfare expenditure used to support the unemployed, and to subsidise the many employers that pay low wages.

But isn’t there too much debt already?

There is certainly too much private debt depressing the economy, making private borrowers reluctant to borrow more for investment purposes. Without investment, there can be no material and sustained recovery. The absence of recovery makes banks reluctant to lend to the private sector, knowing that their customers are largely over-borrowed, and unlikely to make profits/repayments while the wider economy remains below par. This vicious cycle will continue, and can only be ended if the government intervenes.

There are three ways to deal with private debts. They could be inflated away – but that is undesirable. They could be written off, and acknowledged as unpayable, or ‘re-structured’ with lower rates of interest, and with terms extended. Finally, they could be paid down. But they can only be paid down with income. Employment generates income. One of the best ways of dealing with an overhang of private debt, is to create employment and with it, income. Its really not complicated.

But what of public debt?

The British political parties have a near-hysterical and clearly ideological obsession with both the government’s deficit and public debt. The obsession is not so much with the debt, as with the desire to ‘shrink the state’. However the truth is that unlike private debt, government debt is no barrier to action. This is because the government has what no private household or corporation has: a guaranteed source of revenue from taxation from a large population, both now and into the future. This makes the government a very safe, long-term borrower, able to command good terms for its bonds.

Second, the UK government has its own Bank (unlike states in the Eurozone). The nationalized Bank of England can influence interest rates, issue the currency, can act as lender of last resort, and can passively support the government’s bond issuance. It is effectively an arm of government, for all the talk of ‘central bank independence’. By issuing bonds in a process that both supports financial institutions like pension funds and banks; and to have this bond issuance passively supported by the Bank of England, the government would in fact be borrowing from itself, albeit in a roundabout and transparent way – via commercial banks. (If the Bank of England was allowed to lend directly to government – to elected politicians – then all manner of corruption can be envisaged. Zimbabwe’s is an example of a monetary system that is not independent of politicians, is not transparent, and that is not well managed.)

It is because of these undoubted strengths of a well-managed monetary system, that governments with sound institutions can mobilise enormous funds to fight wars and undertake big projects. (Most poor countries lack sound monetary institutions, as developed by advanced economies. As a result they lack money.)

However in order to maintain stability or equilibrium across the economy, it is important for governments to borrow wisely and transparently, and to ensure that borrowing is aimed at productive, income-generating activity – with which to repay debts. If borrowing is aimed at speculation, then it is bound to harm economic activity, by inflating, and then bursting bubbles in e.g. property, commodities, or stocks and shares.

Only an active programme of productive, labour-intensive public investment will, in a slump, shrink the government’s deficit and reduce public debt.

Despite all its best efforts to slash public investment, public debt has risen under the Coalition government’s austerity programme, when it should have been falling in 2014-15. That is because the government has focused on cutting public services and investment, and not on expanding investment, employment and other economic activity, to generate increased tax revenues and cut welfare payments.

As a result of this wrong-headed and ideological approach, Chancellor Osborne has presided over a rise in public debt, and, much to the dismay of its loyal supporters, the Conservative-led government’s annual deficit (the gap between income and expenditure) has remained high. In fact, the deficit is larger than it was over the same time period under the last Labour government. This is all the more remarkable given that during the term of the 2010-2015 Coalition government the economy has not, as under the last Labour government, had to endure a global financial crisis on the scale of 2007-9.

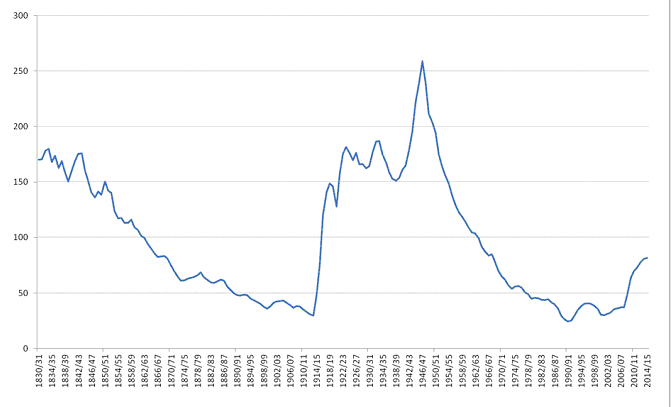

Even so, as the chart below shows (updated from our earlier report: The Cuts Won’t Work) public debt as a share of national income remains low, in historic terms. And as the chart shows too, public debt fell dramatically as part of the post-war reconstruction process. Rises in debt caused by spending on the destructive process of World War II, were halted by post-war productive spending financed by expansionary monetary and fiscal policy. When public spending on job-creating, productive activity rose, public debt began to fall – as sure as night follows day.

Today the challenge to the nation’s security posed by climate change demands the same mobilization of private and public resources as were mobilized then.

Taxing offshore capitalism

It goes without saying that government investment in the Green New Deal can be buttressed in part by increasing taxation of the rich, and by taxing corporations that shunt their profits offshore. These issues have been discussed at length elsewhere so we will not dwell on them here. Suffice to say that sound tax collection plays a vital part in managing the public finances. But the soundest form of tax collection is based on full employment – when millions are working in skilled, well-paid jobs and paying taxes.

Conclusion

Britain, like other advanced economies has a sound monetary system buttressed by institutions like the legal and criminal justice system; the system of accountancy and a semi-independent central bank. It also a large working and tax-paying population, big pension funds and many big corporations headquartered here. As a result, it can easily mobilise the resources needed to fund for example, the Green New Deal. Backed by the Bank of England, these funds can be raised by government issuing a range of bonds – for short, medium and long terms – to be purchased by the commercial banking system. Indeed, given the shortage of AAA-rated assets for purchase by, for example, pension funds, it would be wise of governments to issue long-dated and hypothecated ‘Green Bonds’ – aimed at transforming Britain’s carbon-dependent infrastructure, while at the same time providing safe assets for pension funds.

As we have seen with QE, this borrowing can be passively supported by Bank of England’s monetary operations for transmitting finance and for lowering the rate of interest.

These borrowed resources can be supplemented by more effective tax collection from multinational corporations, from those who own wealth, and from a rapidly expanding ‘green collar’ army of high-skilled and well-paid employees.

But for that to happen requires first a greater public understanding of monetary policy. Second a better understanding of these issues by academic and professional economists, many of them blinded by economic dogma. Third, we badly need a government committed to the transformation of the economy away from fossil fuels, and determined to use the monetary system, not taxation, to finance that transformation.

Above all, we need to challenge the mantra favoured by economically illiterate politicians and commentators: namely, that “there is no money”.

End.

[i] Margaret Thatcher in a speech to the Conservative Party October 1983. Online: http://www.margaretthatcher.org/document/105454 [accessed 1/10/ 2013, 13:06 GMT].

[ii] Bank of England Video: QE – How it works. Banke of England website. Online: http://www.bankofengland.co.uk/education/pages/inflation/qe/video.aspx [accessed 3/10/2013, 11:17 GMT].

[iii] Funding for Lending still fails to deliver, by Geoff Tily, TUC, 04 March, 2015 http://touchstoneblog.org.uk/2015/03/funding-for-lending-still-fails-to-deliver-as-bank-bosses-reward-themselves-while-cutting-back-lending-to-firms/

[iv] Daily Telegraph. General Election Live, by Rosa Prince. 6 April, 2015. http://www.telegraph.co.uk/news/general-election-2015/11517355/General-Election-politicians-hit-the-Easter-Monday-campaign-trail.html

[v] Mervyn King in a conference speech. Sky News Report and Video. Online: http://news.sky.com/story/733003/boe-governor-signals-fragile-uk-recovery [accessed 4/10/2013, 14:08 GMT].

[vi] Ibid.

[vii] Liam Byrne quoted in Paul Owen: Ex-Treasury secretary Liam Byrne´s not to his successor: there´s no money left. Guardian, on 17th May, 2010. http://www.theguardian.com/politics/2010/may/17/liam-byrne-note-successor [accessed 4/10/2011, 14:13 GMT]

[viii] George Osborne, Britain’s Chancellor of the Exchequer on Sky News on the 27th February, 2012. Online: http://www.telegraph.co.uk/news/politics/9107485/George-Osborne-UK-has-run-out-of-money.html [accessed 4/10/2013, 14:17 GMT].

[ix] Ed Balls: Striking the right balance for the British economy, delivered at Thomson Reuters, on Monday 3rd June, 2013. Online: http://www.labour.org.uk/striking-the-right-balance-for-the-british-economy [accessed 04/10/2013, 14:19 GMT].

[x] For more on this, see the Bank of England’s regular reports, Trends in Lending.

[xi] Real Wages and Living Standards: the latest evidence, by Stephen Machin, LSE. http://blogs.lse.ac.uk/generalelection/real-wages-and-living-standards-the-latest-uk-evidence/

[xii] The Distributional Effects of Asset Purchases Bank of England, 12 July 2012

http://www.bankofengland.co.uk/publications/Documents/news/2012/nr073.pdf

[xiii] Why QE won’t resolve the Eurozone’s money problem by Frances Coppola, 08 January, 2015. http://blogs.ft.com/the-exchange/2015/01/08/why-qe-wont-resolve-the-eurozones-fundamental-money-problem/

[xiv] Professor Richard E. Werner Replace Bond Purchases with Solar PV Purchases 8 February, 2012, University of Southampton Management School, Policy News. http://www.greennewdealgroup.org/wp-content/uploads/2012/03/Green-QE-report-CBFSD-Policy-News-2012-No-1.pdf

[xv] The impact of the 2008 rebate by Christian Broda , Jonathan A. Parker, Vox EU, 15 August 2008. http://www.voxeu.org/article/did-2008-us-tax-rebates-work

[xvi] Combatting Eurozone deflation: QE for the people by John Muellbauer, Vox EU 23 December, 2014. http://www.voxeu.org/article/combatting-eurozone-deflation-qe-people

One Response

I agree with much this article by AP, particularly the idea that most politicians are economically illiterate. I disagree on the following points.

The flaw in that idea is that the BASIC PURPOSE of the economy is to produce what consumers want (both private and public sector produced stuff). Thus to deny people the power to purchase more stuff on the grounds that “I” know better, i.e. that money needs spending on investment is a bit arrogant. That’s fine if you’ve done some sort of huge survey into businesses large and small and into nationalised industries and government departments etc, can PROVE that more investment is desperately needed, but not otherwise.

Moreover, I suspect the average business proprietor and manager of sundry government departments (local and nation) have enough brain to know how much to spend in investment each year, without any advice from Ann Pettifor, or me or anyone else. When additional income appears from consumers who are spending more thanks to the helicopter drop, those managers will AUTOMATICALLY allocate a proportion of that to funding new investment.

Shortly after that Ann advocates “labour intensive” types of investment (a slight oxymoron, but never mind). I suspect she has fallen for the popular myth that expenditure on stuff, the production of which is labour intensive creates more jobs than non-labour intensive stuff.

The flaw in that argument is that no matter how you spend £X, ultimately the same number of jobs are created because labour is the ULTIMATE COST. E.g. if one spends on stuff which employs a lot of capital and or materials in its production, that just means that a relatively large number of jobs will be created producing the capital equipment and/or materials. And that capital equipment and materials will themselves need labour, capital equipment and materials for their production. In short, labour is the ultimate cost.

As for John Weeks’s idea that government should borrow billions from commercial banks, I find that bizarre. All that central government does there is to pay banks to make book keeping entries (which produce money) which the state can easily do itself at the click of a computer mouse. Alistair Darling produced £60bn at the click of a mouse at the height of the crisis for the benefit of two failing banks. And the British state produced a lot more than £60bn over the last two or three years at the click of a mouse so as to fund QE.

In short, why pay commercial banks to produce money if you can produce it yourself at no cost?