Graham Gudgin is Honorary Research Associate at the Centre For Business Research (CBR) in the Judge Business School at the University of Cambridge.

The UK Government’s austerity programme is intimately entwined with economic forecasts. The Charter for Budget Responsibility ties the Government into balancing its budget by 2019/20, and the forecasts of the Office for Budget Responsibility (OBR) assess whether the Government is on course to meet this fiscal objective. The political importance of the OBR forecasts is reflected in the fact that the OBR was mentioned ten times in the Chancellor’s 2015 Autumn Statement speech and the Director of the OBR was thanked by name.

The OBR forecasts to 2020 also project the consequences of this fiscal plan, or would do so if there was any feedback from fiscal policy to aggregate GDP in the sense of a Keynesian multiplier. Since there is no such feedback, austerity appears to have no adverse consequences for aggregate output or employment. The relaxed public reaction to the austerity plans, and indeed the Conservative victory in the 2015 general election, are influenced by the OBR’s judgement that fiscal austerity can be combined with favourable economic growth.

The OBR forecasts are driven by supply-side assumptions in the form of trend growth of productive capacity and an assumed rapid convergence of GDP towards this trend. Productive capacity is not measured directly but is assessed as current GDP plus an ‘output gap’ the size of which is measured from surveys of businesses. The future growth of productive capacity is almost all assumption. Assumptions about productivity growth are combined with projections for the expansion of labour supply (where migration depends on ONS assumptions).

Since the UK economy is currently judged to be close to full capacity, the OBR’s forecasts for GDP are the same as its assumed path for productive capacity, i.e. a growth of close to 2.4% per annum, essentially forever. Fiscal austerity makes no difference. Any fall in public spending is automatically compensated for in the private sector, including an unprecedented five-year run of business investment growing at 6% per annum..

We find the OBR’s approach to modelling unhelpful and unrealistic. This approach has a relatively poor forecasting record and, of course, is incapable of projecting a major downturn or crisis except as an exogenous shock. The DSGE model of the Bank of England is in our view even more unrealistic, with a worse forecasting record. As a result of dissatisfaction with these approaches, we have spent the last three years constructing an econometric model of the UK economy following a broadly Keynesian framework, and based loosely on the post-Keynesian ideas of Godley and Lavoie’s ‘Monetary Economics’. A description of the model and the first forecast report are on the website of the Centre for Business Research at the University of Cambridge.

Our CBR model includes the impact of borrowing and debt on household consumption and investment, and recognises the importance of what Claudio Borio of the Bank for International Settlements calls ‘financial super-cycles’. These are credit cycles, which in the UK have tended to last for around 20 years. Our view is that the fourth post-war cycle began in 2012 and it is the upswing of this cycle that is generating the economic growth that offsets the impact of public sector austerity. Our projection is that the cycle will slow over this parliament and peak around 2020.

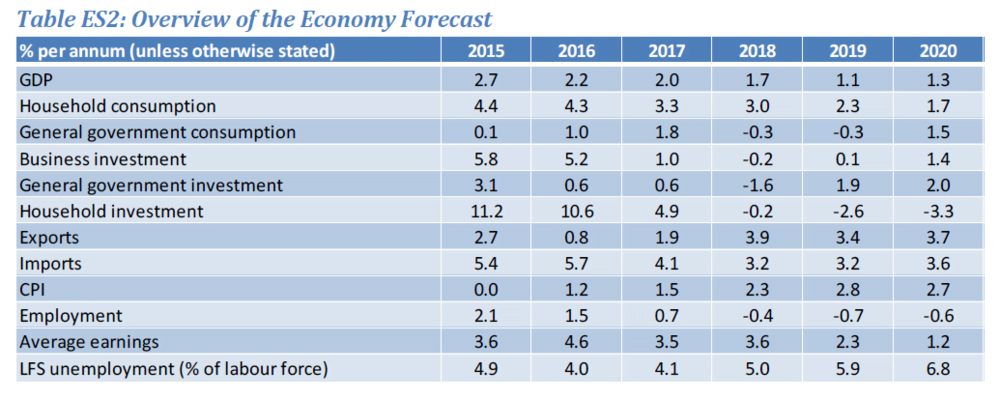

A slowing credit cycle combined with cuts in government spending lead us to forecast that GDP growth will slow to a little over 1.0% per annum by the end of this decade and remain slow there-after. Slow growth in GDP, combined with higher interest rates and the recent upturn in wage growth will, in our view, lead to an end to the jobs boom which has been such a remarkable feature of the UK economy since 2012. Since we do not assume that the UK will leave the EU, our expectation is that immigration will continue at a high level even without much growth in jobs, just as it did in 2009. The combination of low job growth and high immigration means that we expect unemployment to begin rising once more after 2017.

Much of course depends on the wider economic environment. Our forecasts are conditional upon assumptions about the growth of world trade and US interest rates. Since we do not forecast international economic conditions ourselves, we have used Forecasts for UK-weighted world trade from the Oxford Economics world model. OE project an improving growth rate for world trade, rising to 5% per annum in 2017 and 2018 but growing in the longer term at 4% per annum, a rate which is well below the historic average of over 6% per annum. The outcome is almost certain to be more volatile than this forecast, and dependent on unforeseeable political and economic global circumstances. Such volatility would affect the UK’s economic future but not necessarily change the average growth path. For US interest rates we rely on our own assumption that short-term rates will slowly rise to 3% by 2019 and remain at that level. Once again, if the actual path is different the UK forecasts would change.

The slow growth projected in our forecasts would reduce the flow of tax revenues and lead the Government to miss its target for a zero deficit by 2019/20 with public sector debt remaining well above the OBR’s expectation that it will fall to 71% of GDP by 2020. One of Wynne Godley’s beliefs was that governments cannot control their deficits or debt, since their revenues depend on growth in private sector income. In the current circumstances the Chancellor is, in our view, relying on the expansion of household debt to generate the revenues necessary to cut government debt. Our CBR forecasts serve as a warning shot to the Chancellor that although austerity may help to protect the public finances, a consumer credit boom and escalating house prices will lead to yet another boom bust cycle.

Download the whole report here.

The Report was originally published by the University of Cambridge Judge Business School.

The authors of the Report are:

Graham Gudgin, Honorary Research Associate at the Centre For Business Research (CBR) in the Judge Business School at the University of Cambridge. He is also visiting Professor at the University of Ulster and Chairman of the Advisory Board of the Ulster University Economic Policy Centre

Ken Coutts – Honorary Research Associate at the Centre For Business Research (CBR) in the Judge Business School, Emeritus Assistant Director of Studies in the Faculty of Economics, and Life Fellow in Economics, Selwyn College, at the University of Cambridge;

Neil Gibson, Professor of Economic Policy and Director of the Economic Policy Centre at the Ulster Business School at the Ulster University;

Jordan Buchanan, economist at the Economic Policy Centre at the Ulster Business School at the Ulster University.