It is a truth universally unacknowledged that beneath their respective cultural veils, the British and the French are really quite similar. Take, for example, their demography and economics.

The total population size is almost the same. In 2013, the French was around 65.5 million (from INSEE). The UK population was around 64.1 million (from ONS). That makes France’s population just 2.2% greater than the UK’s, and that is mainly due to the inclusion of extra-metropolitan territories for France. Each has an older population (65+) of between 11 and 12 million, with France’s about 400,000 larger.

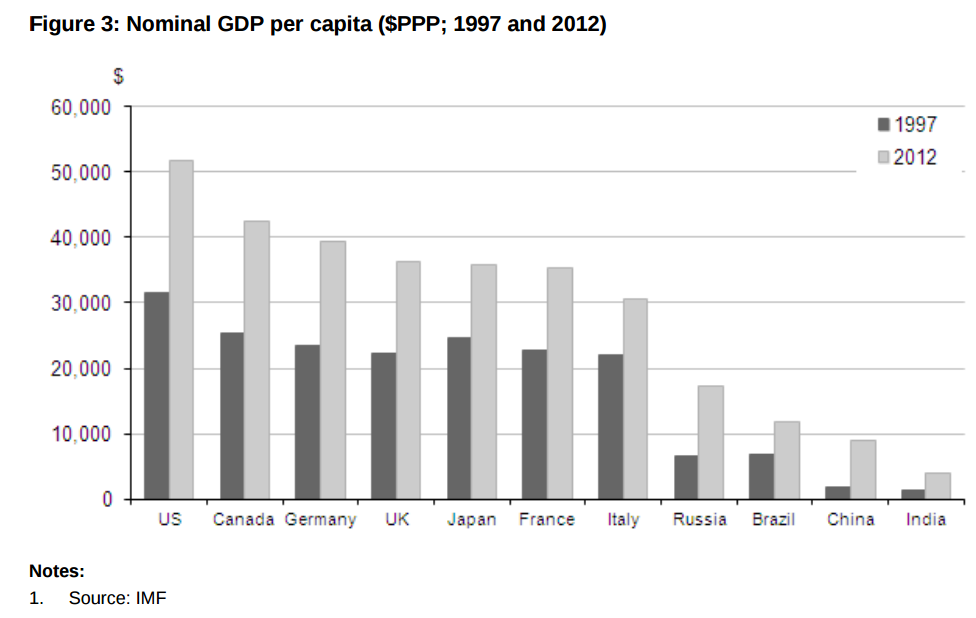

Next, take the size of the economy. In 2012, France’s GDP, translated into US dollars, came to $2,371,906 million, whilst the UK’s for that year was $2,368,261 – an almost invisible gap of 0.09%. That is as near to a statistical dead heat as you can get!

For 2014, the OECD puts France at $2,525,962m, and the UK at $2,552,152m (in current prices and current PPP, or purchasing power parity). The difference is just 1%, but that year in the UK’s favour, reflecting its economy’s somewhat better year than France’s.

In nominal GDP per person, there is therefore another near dead-heat, both for 1997 and 2012:

Or take the structure of the economy – the UK and France each has a manufacturing sector which is 10-12% of the total economy (production as a whole is 15%) while the service sector for each is 79%. The service sector breakdown is also almost identical, e.g. the business services sector is around 29% for each (from BoE).

And last but not least in similarities, both have gaping trade in goods deficits, which added together come to roughly the equivalent of Germany’s trade surplus! Even their net capital stock has risen at the same rate between 2009 and 2015 (UK +8.4%. France +8.1%, faster than other EU members).

But in one area the two countries diverge sharply – in labour productivity, measured in output per hour worked. Here, France and the UK have taken very different paths to achieve, in effect, an almost identical end result. And this is reflected in the very different labour market policies followed in recent decades.

Productivity – from puzzle to crisis?

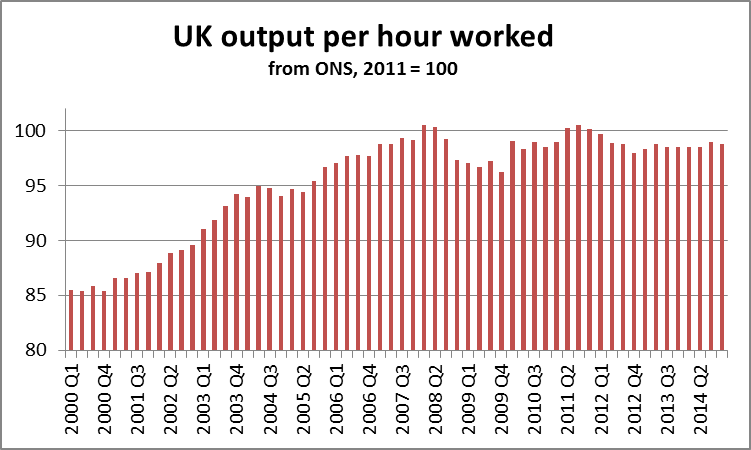

It has been a mystery to most UK commentators why, since the onset of the financial crisis in 2008-9, UK productivity has stalled, even though (or because) at the same employment (as employees or self-employed) has increased. This stagnation of productivity is seen as a danger to our future.

Here is the record, from 2000 to 2014:

In recent days, the Financial Times has run several articles on the subject, full of concern. Chris Giles (the FT’seconomics editor) warns:

Ever since the industrial revolution, economic growth has rested on the firm foundation of better use of buildings and machines and improvements in the level of output for every hour worked. Britain’s advanced economy and comfortable living standards have been built on productivity growth…

According to economists, little is more important than the efficient use of labour and capital. Over a decade ago, Paul Krugman, the Nobel prize-winning economist, famously said: “Productivity isn’t everything, but in the long run it is almost everything”.

Per capita hourly output is not prominent in any electoral literature, but Britain’s deficit and cost of living problems will overshadow politics as long as productivity remains weak. [my emphasis]

But is all this current concern well-targeted? Or more pertinently, is the productivity problem a principal cause of our difficulties, as the FT seems to think, or mainly a symptom or effect of other problems? This is where the comparison with France – and indeed with other G7 countries – is especially interesting.

The UK in international productivity comparison

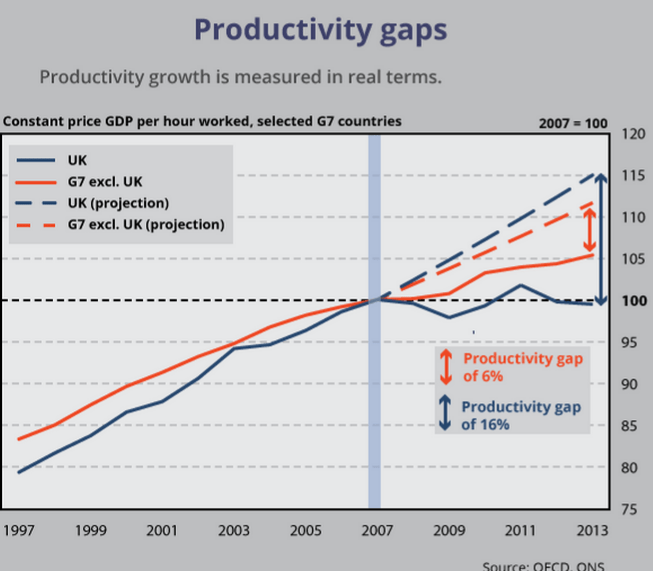

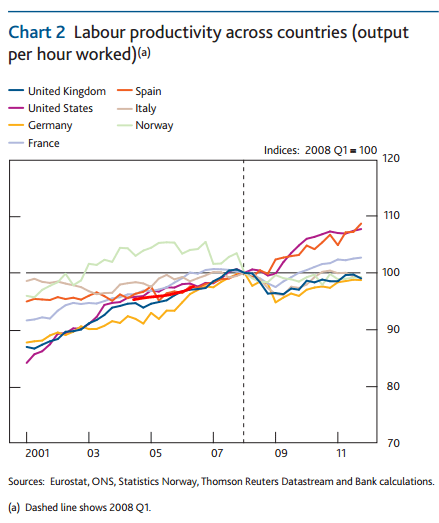

The UK has long had lower labour productivity than all other G7 countries bar Japan, but the gap had been narrowing gradually. Since 2007, all G7 countries have suffered slower than trend productivity growth, and the UK has slipped back relatively again:

But some G7 countries have been doing slightly better – the US and Germany for example – whilst others like the UK, France and Italy have stagnated. The Bank of England chart, below, shows the relative performance of several countries here, with 2008 = 100. (Please note this maps each country’s own performance, and does not show absolute levels of productivity).

The two best “improvers” on labour productivity post-crash are therefore Spain and the US – yet Spain suffered a decline in GDP and astronomical unemployment! Clearly, higher productivity is not always a positive feature! The UK and Germany have run (or stagnated) in parallel, notably since the Hartz reforms in Germany which rendered the German labour market more “flexible” – and of the large EU countries, Germany and the UK have seen the most new employment added.

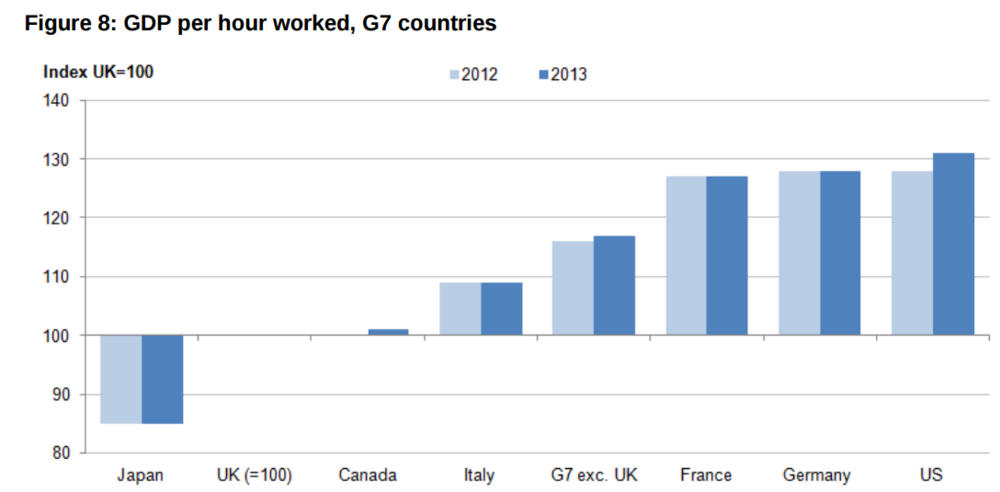

The relative positioning of the UK is clear from this ONS chart, which shows France, Germany and the US almost on a par, around 30% better than the UK:

Because the UK produces the same output as France, it follows that UK workers work many more hours than their French counterparts, but the value of their hourly output is much less. The OECD statistics bear this out ; for 2014 the GDP per hour worked was $50.5 for the UK, but $62.7 for France (Germany, out of interest, was $62.3). So France’s GDP per hour worked is about 25% greater than the UK’s! (All in current prices, current PPP).

So in sum, France produces roughly the same output, year on year, as the UK, yet does it by working far fewer hours than workers in the UK, producing far more per worker than the UK, and having in general a far higher unemployment rate over a sustained period:

The usual gap between the respective unemployment rates of France and the UK is therefore some 2-3% – meaning between 500,000 and a million more unemployed in France on average.

This is at least partly explained by the degree of deregulation of the labour markets. The UK’s is an extreme form of deregulation, which enables employers more easily to make workers redundant, to reorganise, downsize, casualize (zero hours etc.) and to reduce wages; the French system is in effect the opposite, with far stronger rights for those in employment, and in general a stronger social protection for those out of work. (It is also true that setting up one’s own business, including small businesses, in France is harder than in the UK).

So is the main problem productivity?

We are faced with a key question – is it a coincidence that the economies of the UK and France, over a sustained period of decades, have run in so many respects in parallel, with overall output and GDP (including GDP per head at PPP) at remarkably similar levels? In particular, is it a coincidence, given that the labour market means of arriving at this similar result are (since the early 1980s) so divergent? Or is there some other factor at play, which could explain both the similarity and the result?

Assessing and comparing national productivity

Let us first look at whether – viewed from a national, rather than company, perspective – we are correctly assessing what “productivity” means. Does it measure the output per hour or per worker of those in work? Or does it measure the output per hour, or the output per worker, of the whole labour force – employed and unemployed alike? (For output, GDP is the simplest number to use here).

In a company, if you employ 10 persons but only 9 are at work for the time being, the 10th still being paid, the firm’s productivity is partly measured by the output per hour of the 9 (who may or may not be doing overtime), but in terms of output per worker, the 10th will be included in the calculation. Here it is the whole workforce that counts.

At national level, the entire maximum labour force consists of those in employment plus the unemployed (i.e. the economically active) plus any element of the economically inactive who might be induced, in good times, to enter the labour force.

In the UK, the current economically active rate is at a historically high level (December 2014-February 2015) of 79.9%, of whom 73.4% are in employment (or self-employment). This indicates that 80% would be a reasonable “total workforce” estimate, though it could go a little higher.

In France, the percentage of economically active has generally been lower than the UK, the employment rate in Q4 2014 being 64.2% and the unemployment rate 10.4%, making a total of economically active of 74.6%. It is reasonable to assume that the potential workforce is higher than this (if full employment were ever approached), but possibly a little lower than the UK.

But for ease of calculation, let us first simply divide the population of each country by the number of economically active.

In France, for Q4 the number of economically active was 28.365 million, and the 2014 GDP $2,525,962 (in current prices). This makes the GDP per economically active person $89,052.

In the UK, the number of economically active for Q4 2014 was 32.758, and the 2014 GDP $2,552,152m. This makes the GDP per economically active person $77,909. Still a gap (of 14%), though much less than that for GDP per hour worked or per in-work worker, where the French have a productivity lead of near 25%.

But if we next assume – surely reasonably – that the potential French labour force is greater, and add (say) half the difference (+2.2m) between the two countries’ economic activity rates, we get a total workforce for France of around 30.6 million. The GDP per economically active person would then be $82,557 – much closer to the UK (a difference of 6%).

And of course, if we assume the same potential economically active number for France as for the UK, then there is almost no gap at all! The GDP per member of the French labour force would be $77,110.

In conclusion, looked at from a national labour force perspective, the productivity gap between France and the UK almost disappears!

The French problem – demand not productivity

It should be evident by now that – whatever problems the French economy has – these do not include productivity per hour worked, or per worker. Yet no one considers that the French economy is currently working at or remotely near full potential. With an unemployment rate of over 10%, it would be crazy to claim so. The answer to the French problem, it is said, is major structural reform, especially to the labour market.

As someone who has employed staff (on a small scale, with non-profits) in France, Belgium and the Netherlands as well as in the UK, I do – from experience – consider that the employer’s task in France is excessively onerous (financially also) and uncertain. So some labour law reforms – up to a point – may be beneficial for the long run.

But the French would be equally crazy to go to the British extreme, which simply bolsters and reinforces the low pay, low security, low productivity system governments have so lovingly created. (Or as the FT puts it, capital and labour in the UK have been “deregulated to a sensible degree”!)

What is obvious about France is that, to create full employment without undermining productivity levels, demand would need to be increased greatly (whether domestic demand, or greater demand for French exports – which means action also by Germany). The French government has been reducing its budget deficit, which is lower than the UK’s, but even so this has further damped down demand in the economy.

If you deregulate labour and take other steps without increasing demand, especially via investment, then labour productivity in France will fall, not rise. Supply-side measures do not create their own increased demand, even if some can help a country to benefit from increasing demand when the opportunity comes.

And what about the UK productivity problem?

The FT and other commentators are however convinced that the UK’s productivity only needs supply-side measures, despite its already highly deregulated labour market. Chris Giles argues that “low-hanging” fruit include deregulating the market in land, new airport runways, and simpler tax system. Other articles cite (as factor or obstacle) today’s more time-consuming regulatory measures (e.g. on money laundering) now in place for business services.

Once again, the elephant in the room is the shortfall in demand. Governments as well as other sectors have been trying to deleverage. Real pay fell by at least 8% since the crisis began, which has greatly reduced spending power, and thus demand, in the economy. This has not been mitigated by a much-improved trade or current account balance – we remain steadfastly in deficit. Geoff Tily, the TUC’s senior economist, underlined this point about demand in his New Statesman article of 5th March:

Arguing that we can only have growth and better living standards as a result of productivity increases gets the argument exactly the wrong way round. The truth is that investment and increases in demand and an end to austerity economics will inevitably boost productivity – and with the right supply-side policies to ensure growth is fairly shared and that investment can get a good return can deliver a virtuous circle where demand boosts productivity which in turn produces more growth.

If there is a puzzle, it is why so much of the economic establishment has neglected the demand side. When we have severe austerity, reduced economic growth but sustained employment growth, even if on the back of painfully low wages, it is simple arithmetic to see that productivity must suffer.

He cites the 2012 detailed academic work by Martin and Rowthorn who also concluded that

The UK’s poor productivity is more plausibly interpreted as a symptom of a largely demand‐constrained, cheaper labour economy ‐ a condition misinterpreted by supply pessimists as a sign of structural weakness. Output is well below potential because workers, while cheaper to employ, are not working to potential. More output could be produced, but not sold. There is an effective demand failure, high unemployment and, within companies, under‐utilisation of the employed workforce – a form of “labour hoarding”.

It is true that domestic “demand” has recently slightly increased (though the latest retail figures show a year on year rise of just 0.7% in value) but much has had to do with increased volumes which have not translated into similarly increased turnover. Real pay is at last increasing, but very slightly (just over 1.3% annual rise in total pay recently), and even that is mainly due to the economy’s flirtation with deflation.

It is clear that – despite the sharp fall in headline unemployment – there is still significant slack in our labour market, and in the productive use of labour.

Low productivity – by-product not cause of low economic activity

As we have seen, the French and UK economies are extremely similar in many important respects, including their sectoral structures and weighting, and this has led to very similar outcomes in terms of overall GDP and GDP per head. Although France faces particular problems at present as a member of the troubled Eurozone, both economies are subject to similar economic forces, including international factors.

Being much the same size, as economies and populations, the domestic spending power in each country is broadly similar, and this leads to similar levels of overall demand.

In recent years, both have undergone sharp austerity programmes aimed at reducing deficits as a percentage of GDP – and both governments are promising more. Even if neither austerity programme has gone – or succeeded – quite as far as some wanted, both have had the effect of reducing aggregate demand.

The two countries differ however in their policies for sharing the pain, or dividing the cake, whichever metaphor you prefer. The UK has gone for a higher employment, lower productivity solution; France the opposite. Both are currently more or less stuck at their existing productivity levels; but both have had very low increases in GDP in recent years (save the better UK result in 2014).

Improving productivity via demand

One important answer for the UK is to increase pay – notably by a significant and early rise in the minimum wage, and bringing back reasonable job security, as well as treating phoney self-employment as real employment (with its attributes). It is high time for government to stop subsidising employers for paying very low wages.

Even more importantly, investment must be increased – and the government should not be the least bit squeamish about borrowing for genuine capital purposes, for the country’s future. This investment, and the jobs it creates, should also be targeted to helping the transition to the post-carbon society and to universalise (including rural areas) the development of the connected society.

For France, the answers are more complex, since the Eurozone’s rulebook, with its obsessive obsession with inflation and deficit-avoidance (i.e. austerity) over all other goals, is not designed to promote high levels of economic activity. Unless and until the rules are greatly changed, or (as is really necessary if the Eurozone is to survive into the long term) there is a politico-fiscal union, the going will be tough for France.

There is – as Laszlo Andor has pointed out here – a need to have an effective investment programme for the EU, which the Juncker plan scarcely provides, and as indicated above, there is a need to adjust France’s traditional labour market model to promote more job creation.

But the Eurozone as a whole needs to turn its back on austerity (and its other obsession, generating external trade surpluses rather than internal development) if France, as well as others, is to thrive once more.

This is not to deny the importance of some so-called supply-side measures – improved education and training for example; but the answer does not lie in ever more deregulation of ever more sectors, allowing capital to do whatever it wills. But the relentless emphasis on supply rather than demand is a sign more of economic ideology than of economic analysis.

What essentially unites the two countries’ economies is a lack of demand and economic activity sufficient to generate full employment (especially in France) at reasonable wages (especially in the UK). The productivity “solutions” each has found, however opposite they appear, are merely responses to similar pressures.

France values education and training. It also gives holidays a sacred status*. Both result in higher productivity per worker and per hour worked. French bureaucracy is infuriating, but it costs less than it agitates: regimes are easier for " very small companies" and big ones have experts in navigating it. France is having more problems than most ( especially the UK) with the EU austerity philosophy and of course more with EZ austerity. Germany values France more than the UK, but has so far resisted French attempts to relax austerity. Brexit may change that!

Writing this on a Tuesday bank holiday where companies and government of offices were closed on Monday as a "bridge" to the weekend, and smaller businesses will take tomorrow off.

A bitcoin for good complementary currency that is earned into existence for pro-social or pro-environmental activity will deal with this productivity gap since it will provide increased liquidity for assets that are under-employed.

Such as people, empty shops or seats on buses.

It’s all very well for you economists to bang on about productivity and growth, but what’s the cost?

What we don’t need is more of the same growth as measured by GDP, we need sustainable growth and produces the stuff people demand – more community, more happiness, better health, more affordable goods and products, a cleaner environment.

A bitcoin for good would set the standards for a new global currency that is universal in nature and 100% sustainable – and a new way of measuring success that rewards collective action that benefits everyone.

Check out Hullcoin if you think this is all hot-air.

2 Responses

France values education and training.

It also gives holidays a sacred status*.

Both result in higher productivity per worker and per hour worked.

French bureaucracy is infuriating, but it costs less than it agitates: regimes are easier for " very small companies" and big ones have experts in navigating it.

France is having more problems than most ( especially the UK) with the EU austerity philosophy and of course more with EZ austerity. Germany values France more than the UK, but has so far resisted French attempts to relax austerity. Brexit may change that!

A bitcoin for good complementary currency that is earned into existence for pro-social or pro-environmental activity will deal with this productivity gap since it will provide increased liquidity for assets that are under-employed.

Such as people, empty shops or seats on buses.

It’s all very well for you economists to bang on about productivity and growth, but what’s the cost?

What we don’t need is more of the same growth as measured by GDP, we need sustainable growth and produces the stuff people demand – more community, more happiness, better health, more affordable goods and products, a cleaner environment.

A bitcoin for good would set the standards for a new global currency that is universal in nature and 100% sustainable – and a new way of measuring success that rewards collective action that benefits everyone.

Check out Hullcoin if you think this is all hot-air.