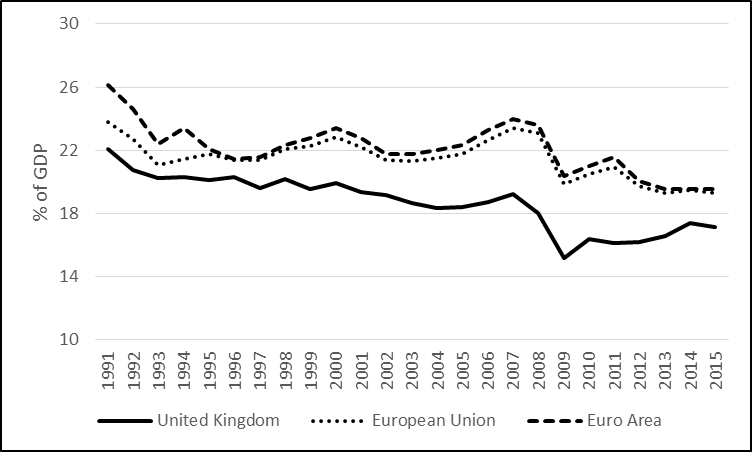

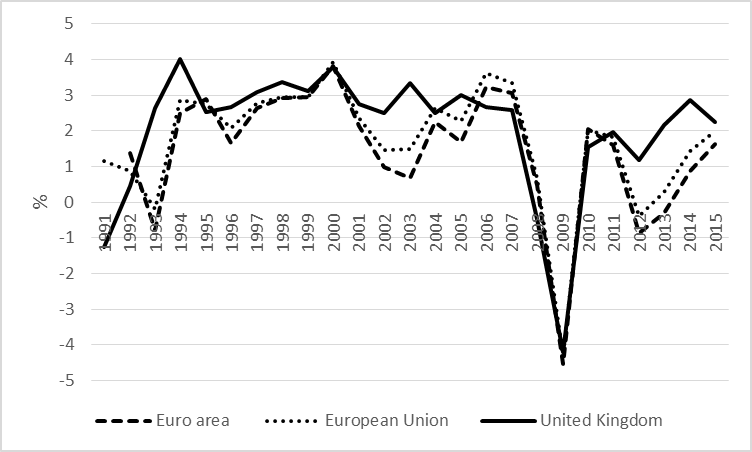

Low investment has been dragging down growth and industrial development across Europe. Even in countries like Britain where GDP growth is currently above 2% (figure 3) it is questionable whether a recovery not based on the expansion of investment, especially on innovation and technological transformation, is going to be sustainable in the medium run (Griffith-Jones and Cozzi 2016).

Figure 4, GDP growth

Source: IMF World Economic Outlook (updated April 2016)

Britain has adopted a growth strategy that tries to circumvent this crucial problem of low investment, and instead it has sought to revive demand largely by increasing consumer debt. The Office of National Statistics (ONS) reports that during the period July 2012- June 2014 aggregate mortgage debt in Britain stood at £1,057bn, up from £960bn in the period July 2006 – June 2008. Further, ONS reports that the median amounts outstanding for household non-mortgage borrowing increased from £2,900 in the period July 2006 – June 2008 to £3,700 in the period July 2012 – June 2014.

To reverse these worrying trends powerful action will be needed. The key to recovery and positive structural transformation in Britain is a significant increase in investment, particularly if linked to innovation and transformation towards a greener and more caring economy. Sustained investment is necessary to incorporate innovative technologies and reignite productivity growth. In a world with growing globalization and increasing competition, de-industrialization and sustainable growth can only be reversed through higher investment and increased cooperation and coordination at European level (Griffith-Jones and Cozzi 2016).

The current policy framework

The current policy framework in Britain (but also across Europe) has been characterised by the orthodox economic view that fiscal austerity leads to an expansion of economic output. As a result a series of harsh cuts to government spending have taken place in Britain since the outset of the global financial crisis.

The justification for this approach rests on the idea that public investment does not boost demand because it merely crowds out private investment, as government borrowing leads to higher interest rates and taxation (Griffith-Jones and Cozzi 2016). However, in an environment of low private investment and interest rates at record low levels, the case for “crowding out” is particularly weak.

Indeed, Stiglitz (2012) argues that public investment, particularly in infrastructure, is likely to ‘crowd in’ private investment and that Infrastructure investment, such as in energy, transportation and telecommunication, creates demand in the short term for a wide range of goods and services in constructions and installation supply chains, and in the medium term it stimulated growth through an expanded stock of physical capital and greater efficiency.

In parallel to cuts in government spending – in particular on welfare and other crucial social infrastructure investment (i.e. in those assets that are focused on improving human capabilities and quality of life, such as investment in nurseries, community housing, and other public services providing care, health, education and training) the British government has made a small attempt to increase investment in infrastructure in order to revive the British economy.

A significant part of this small attempt to increase investment in Britain comes from the European Investment Bank (EIB) which, as a result of the European Fund for Strategic Investment Initiative (EFSI), has increased lending for investment to Britain by £735 million in 2015 – equal to one-third of all EFSI supported lending in 2015 (HM Treasury 2015).

In total only in 2015 the EIB lent to the UK approximately £5.8bn for infrastructure projects such as the upgrading of existing lines and station of London underground system, support to Rolls Royce for the development of new aero engines, campus investment and expansion at Oxford University, constructions of a new children’s hospital in Edinburgh, and various energy efficient projects through the UK for a value of £380 million. Overall, investment in Britain accounted for over 11% to total EIB lending in 2015 (and the total contribution from Britain in terms of called up capital in the EIB is equal to 3.4 bn Euros).

This is a positive although very small step to revive investment in Britain. A greater investment plan, accompanied by strong and effective industrial policies are needed both at national and European level to bring the British economy towards sustainable growth and to revive a declining industrial sector. However, it is clear that Britain also needs European resources to support its economy and stimulate investment and that a vote to leave the European Union (EU) might lead to a significant reduction in the support that Britain receives from European institutions to stimulate investment.

If Britain left the EU, although current EIB projects would continue it would be very likely that the scale of investment in Britain from the EIB would significantly reduce. This is because outside the European Union the EIB predominantly lends to developing countries rather than other developed countries. In addition, an exit vote might lead to increased uncertainty which could negatively affect private investment. Britain needs an alternative strategy for achieving sustainable economic recovery, but not one which brings Britain outside the European Union.

An alternative proposal for sustainable recovery

In order to achieve a sustainable economic recovery, Europe and Britain need a major boost in investment in both physical and social infrastructure. This translates to the need for additional investment measures to those already existing at EU and national level (such as for example the Investment Plan for Europe) and to the recognition that public investment is essential in order to crowd in private investment.

Higher investment in Britain, and across Europe, could be achieved by an expansion of lending by the European Investment Bank, based on an increase in its paid-in capital provided by EU members, including Britain. The EIB’s ability to leverage its own financing to attract private co-investment enables a significant economic impact to be achieved from fairly limited public resources (Griffith-Jones and Cozzi 2016).

Since 2013 the EU has doubled the EIB’s paid-in capital. This has led to a significant increase in lending both in Britain and across Europe. Assuming a leverage ratio of eight, as accepted by the rating agencies to maintain the bank’s triple-A status, an extra 10 billion Euro of paid-in capital would allow the EIB to expand its lending by up to 80 billion. Given that the EIB-funded projects are typically 50% co-financed by the private sector or by national development banks, this might result in additional investment of around 160 billion Euros across Europe (approximately £120 billion). On the basis of the current geographical distribution of the stock of loans of the EIB Britain could then see its investment increase by approximately 13 billion Euros (approximately £10 billion) as a result of such a further increase in EIB paid-in capital.

In addition, the British government should create a national development bank in order to support domestic investment and technological transformation and to complement the lending of the EIB. There are several cases of successful national development banks that have supported the development of domestic infrastructure and the transformation towards a more sustainable and greener economy. In Germany, for instance, the national development bank KfW lends approximately 50 billion Euros per annum for domestic purposed and for innovative projects. A similar state bank could be set up in the UK to support investment in innovation, renewable energies and environmental technologies, physical and social infrastructure, and Small and Medium Enterprises (SMEs).

With regards to the financing of such a state bank in Britain, Skidelski et al. (2011) argues that the British government could either issue gilts to be bought by the market and/or the Bank of England, or it could use the profits from selling its equity stake in commercial banks such as RBS and Lloyds.

Further, in a world with growing globalization and increasing competition, sustainable growth can only be achieved through higher investment in social and physical infrastructure and by making Europe become a much more coherent and coordinated economic (and political) area. In this respect, Mazzucato (2016: 117) highlights the importance for Europeans to learn to cooperate, “to rely on each other and to allow a certain division of labour” between European countries:

“We should let Greece do solar panels, Germany machine tools, Italy art, the UK science – not exclusively but to some extent, with this division of labour, Europe could become a competitive hub” (Mazzucato 2016: 117).

Thus, we should all think how Europeans can work together using and complementing our national capacities, capabilities and tools. Only by a common and coordinated European strategy will we be able to bring Britain and Europe onto a more sustainable economic trajectory.

Dr Giovanni Cozzi is a senior lecturer at the Greenwich Political Economy Research Centre, University of Greenwich

References

Griffith-Jones, S. and Cozzi, G. (2016). “Investment-led growth a solution to the European crisis” in Jackobs, M. and Mazzucato, M. (eds), Rethinking Capitalism: Economic Policies for Equitable and Sustainable Growth. London: Wiley-Blackwell

HM Treasury (2015). “New figures show record European Investment Bank investment in UK in 2015”.

Klär, E. (2014). “Die Eurokrise im Spiegel der Potenzialsähtzunger”, Wiso Diskurs, Friedrich Bebert Stiftung, April 2014, pp. 31-33.

Mazzuccato, M. (2016). “The Myth of the ‘Meddling’ State” in Cozzi, G. Newman, S. and Toporowski, J. (eds) Finance and Industrial Policy. Beyond Financial Regulation in Europe, Oxford: Oxford University Press.

Skidelski, R. Martin, F. Wigstrom, C.W. (2011) “Blueprint for a British Investment Bank”, Centre for Global Studies. (Accessed 25/05/2016).

Stiglitz, J. (2015) “Stimulating the Economy in an Era of Debt and Deficit”, The Economists’ Voice, March (Accessed 25/05/2016)