With the Labour leadership campaign exciting a lot of interest, we thought it would be helpful (we have not seen it done elsewhere) to set out the views of the candidates, in their own words, on macroeconomic and fiscal policy. Of course, those voting will not only take economic policy into account when deciding whom to vote for – but it is certainly an important factor. Especially since George Osborne has – so far and for so long – been allowed to frame the economic debate on his own (heavily political) terms with much success.

We cite each candidate, taken in alphabetical order. Some have spoken or written at much greater length than others – we provide readers with the links to each of the main sources we have found. Please let us know if we have missed any – we would happily correct or add to what follows!

I have also put some passages from the candidates in bold, where they deal with the issue of responsibility for the crisis, with deficits and debt, and with the economic record of the last Labour government. This is not because other aspects are unimportant, but because the approach to the political framing of Mr Osborne (“you can’t trust Labour with the economy”) rests on these pillars.

Andy Burnham

On 15th July, Andy Burnham made a lengthy speech, “A Labour Vision for a New Economy” which covered a broad range of subjects. We recommend readers to read it in its entirety. Here are some key extracts (themselves quite long!):

So now seems the right moment for me to set out what I believe is a better vision for our economy.

As Leader I will work every single day to re-establish Labour as the Party of work, both employed and self-employed, the Party of business, small, medium and large, and the Party of economic credibility.

Today, I will set out the key components of my vision to do that.

A Labour vision with fiscal responsibility at its heart and where growth helps reduce our national debt.

Where government works in constructive partnership with business and unions, not picking fights with one or the other.

Where we rebalance business taxation to take taxes off businesses starting out and on the way up.

Where a high-skilled and high-paid workforce contributes to and shares in our national success, and where the millions of self-employed people are better recognised and supported.

And where we get on and deliver the infrastructure and new homes that our country needs.

But, the hard truth for my party is that George Osborne wouldn’t have been setting out a Conservative Budget at all if Labour had been trusted to set out the alternative.

So, I also want to talk about the fundamental problem facing my party – winning back the trust that we lost back in the financial crisis.

That loss of trust has now cost my party two elections. It will cost us a third if we do not address it. And perhaps more importantly it has taken Britain back to a decade of Conservative government.

Our response now and in the years to come must be driven by a burning desire to win back trust. If I am elected leader, winning that trust will be central to my leadership and that of my team.

My argument today is that we will only win back that trust by being straight with people about our past in government, about the challenges Britain today faces and about our plans for the future.

There is no substitute in politics for being direct with people – and trust comes from people knowing that you will be straight with them and do what’s right even when it’s unpopular.

So today I set out five clear principles that I believe should be at the heart of Labour’s vision for delivering a UK economy fit for the future and fit for the British people.

First of all, a balanced and sustainable economy must be based on balanced and sustainable public finances.

And the trust we seek to regain can only come with a true account of our record in Government.

We achieved many great things but we can see now that it would have been better to have been spending less in the run-up to the crash.

It wouldn’t have prevented it.

Our investments in public services didn’t cause the global financial crisis.

But it would have meant we were in a stronger position to deal with the consequences.

That is not an easy admission for Labour to make, but it is a fair one. And it is necessary if we are to win back the confidence of people….

I believe this honesty about our past is necessary to move forward, but on its own it won’t build credibility or provide answers for the future.

On the eve of the financial crisis national debt had been reduced to just 37% of GDP by the last Labour government, and we had run more surpluses than the Tories had managed to in 18 years.

The deficit we were running was small by historical standards.

And, as I said at the start, I want to be clear that Labour spending on education and the health service didn’t cause the global banking crisis.

I am proud of our legacy on the NHS with public satisfaction at a record high and waiting times at a record low. And I’m proud that we rebuilt thousands of schools and colleges and raised educational standards.

But, small though it was, we were still running a deficit at the peak of a booming economy.

That is why I began my leadership campaign by acknowledging that in government we should have done more to control spending in the middle of the last decade, so that we were better prepared when the crisis hit….

The question facing Britain in the future is how to clear the deficit and run a surplus without making the mistakes of either the last Labour government in overestimating growing tax revenues, or the mistakes of George Osborne’s first term in which savage cuts stifled growth and set back deficit reduction.

Last week’s budget, which disproportionately hit families in work, is no answer to this question.

Labour under my leadership will always run sound public finances and we will reduce the national debt, back toward its sustainable pre-global financial crisis levels.

But we will ensure that growth is as important in our plan as being careful on spending. And what we spend money on will be as important as how much we spend.

We will ensure that delivering long term public spending on investment is never sacrificed for short term political convenience.

I will therefore give the Office of Budget Responsibility the role of regularly auditing government’s investment plans, to ensure enough is being spent on the long term projects that will grow the economy and most effectively reduce our debt levels, while raising living standards….

A true partnership with all types of businesses and the self-employed will inform my approach to the other elements of my vision.

That is why I will also look to work with business on my third principle; a pro-growth rebalancing of business taxes

I will as leader appoint an independent commission on business tax reform, to ensure that the tax system supports those who are starting out and those who are trying to grow their business.

Osborne claims that his budget measures fall on those with the broadest shoulders. But just as it is untrue of his personal taxation and tax credit changes, so it is untrue of the UK’s business tax regime.

It must be in the interest of both businesses and the wider economy that taxes are kept low on those struggling to start up and grow, with those who are established taking their fair share of the burden.

Such an approach will help grow the overall tax base and create more jobs – reducing demands for welfare spending – all of which will lower the tax burden for all in the longer term.

Yvette Cooper

We have not been able to find a recent speech or article by Yvette Cooper that deals with macroeconomic policy specifically. On 8th July, she made a speech “A budget that betrays working parents” in which she said:

Of course the deficit and the debt need to come down. Of course Labour would have had to make tough decisions to get back into surplus. That is why I identified £800m in savings in the home office budget whilst protecting frontline policing- from things like abolishing Police and Crime Commissioners. But it is also why I think George Osborne’s plan to cut inheritance tax now for some of the richest estates is the wrong priority.

Because there is an alternative to George Osborne’s plans. The Tories’ approach isn’t fair, and isn’t good for our economy and our country in the long term.

At the same time as hitting Britain’s families, the Tories are failing to deliver the balanced growth and high paid jobs we need for the future – that also helps bring the deficit down.

Growth has been revised down this year. So have exports. And so has productivity. That means we’re not getting the high skilled jobs our country needs. We need a national mission to almost double R&D investment in our economy to match the 3% of GDP our competitors invest and there were no measures in today’s budget to do that…

At the same time as hitting Britain’s families, the Tories are failing to deliver the balanced growth and high paid jobs we need for the future – that also helps bring the deficit down.

The Chancellor talks about one nation – but he doesn’t think parents are part of that one nation. He talks about a long term plan but he is happy for stagnant growth with weak exports and low productivity to drag our debt up and our economy down.

Labour needs to have the strength to stand for a better approach – for a stronger economy with sustainable public finances and a fairer, less divided country: the two things go hand in hand.

On 15 July, in an article in the Huffington Post, she wrote:

[T]he welfare system still doesn’t work effectively enough to support work and security in the modern world. People are worried about the welfare system at the moment and the Tories exploit those concerns to try to justify cutting tax credits in this way. Budgets are also going to be tight while we get the debt and the deficit down, so we have to look for savings wherever we can.

That is why Labour called for a higher minimum wage and living wage in the first place, saving money as well as getting employees and better deal. So we should welcome the Government’s planned increase at the same time as calling on them to go further for young people who have so far been left out. And it’s why we have long argued for more housing to stop the housing benefit bill going up and up.

Ms Cooper is also quoted (source: Politics Home) as having said, on BBC Radio 4 News at One (13th May):

The deficit at the time was 0.6%, the current deficit, and all the political parties at the time were all supporting the spending plans, and that was all due to come down.

But I think there’s been a focus on that as if that was the economic issue of the time, and the real economic issue of the time was that we had banks who were involved in huge private lending that nobody had spotted the scale of; private sector debt that had been growing up that was unsecured; the links between the financial sector all over the world, particularly into the housing market crisis in America, because if you remember it started with those bad loans in America that then shot across the world.

Jeremy Corbyn

Jeremy Corbyn has set out his position on economic policy in two places – first, and more briefly, in an article in The Independent on 31st July which though entitled “The Robin Hood Tax is a more sensible and fairer way of helping our economy to recover” partly covers a broader remit; and second, in an 8-page policy document “The Economy in 2020”. Again, please read the full document to get the full picture. First, from The Independent:

[The Financial Transactions Tax] is based on two very simple concepts. The first, as the name suggests, is based on the idea that the rich should contribute a little more to stop the suffering of the poorest; and secondly the economic reality that it was the reckless behaviour of the finance sector that got us into this mess and they should be paying for it.

If we cast our minds back almost eight years, to September 2007, customers were not queuing out of the doors of Northern Rock branches because a Labour government had spent too much on nurses and teachers. Just two weeks before, George Osborne had backed Labour’s spending plans.

Labour does have some responsibility for the crash. Not because we spent too much, but because we didn’t regulate enough….

We are still paying for the last crisis, and yet there are fears in the bond markets and in the housing market that things are becoming unstable again. As these warnings become louder, Chancellor George Osborne has made a concerted effort to resist any regulation on the finance sector, and in his recent budget announced that the bank levy will be wound down – even as he announces further welfare cuts for the poorest.

His policies of pay restraint, house price inflation and a reliance on rising consumer debt look to be setting the scene for another slowdown, if not worse. As the party funded by hedge funds, it is no surprise that this most ideological of chancellors has appointed a hedge fund partner to the vacancy on the Bank of England’s Monetary Policy Committee.

The monetary levers that bailed us out last time will not be available again. Interest rates are already at zero, the Bank of England has already poured £375 billion into its quantitative easing, and we are running a larger deficit with more debt than in 2007.

The route to recovery for all cannot rely on the systemically reckless speculation of the City of London…

And next, here are some key extracts from his policy paper (as with speeches etc. of other candidates, we encourage readers to read the whole thing):

Wealth creation is a good thing: we all want greater prosperity.

But let us have a serious debate about how wealth is created.

If you believe the Conservative myth then wealth creation is solely due to the dynamic risk-taking of private equity funds, entrepreneurs or billionaires bringing their investment to UK shores.

So if we follow the Conservative’s tale then it is logical to cut taxes for the rich and big business, not to bother to invest in the workforce, and be intensely relaxed about the running down of public services.

But in reality wealth creation is a collective process between workers, public investment and services, and, yes, often innovative and creative individuals.

Understanding this means getting to grips with the key choice in the leadership election and indeed the key choice facing Britain:

Whether to accept austerity or whether to break free of this straitjacket and strike out for a modern, rebalanced economy based on growth and high quality jobs.

Labour must create a balanced economy that ensures workers and government share fairly in the wealth creation process

- that encourages and supports innovation in every sector of the economy; and

- that invests in skills and infrastructure to build an economy that is more sustainable and more equal.

The purpose of this document is to set out some of the key parts of that vision. That includes not only the overall approach we must take to the economy as a whole, but some specific key changes on taxation.

But look deeper and Osborne’s Budget and a familiar story emerges: tax cuts at the top. This time for the 4% who currently pay inheritance tax, and then for corporations again. And who bears the brunt?

Once again it’s low income families, disabled people, young people, public sector workers, and our public services.

So we see that austerity is about political choices, not economic necessities.

There is money available:

The inheritance tax changes will lose the government over £2.5 billion in revenue between now and 2020.

What responsible government committed to closing the deficit would give a tax break to the richest 4% of households?

The Conservatives are giving away to the very rich twice as much as reducing the benefit cap will raise by further impoverishing the poorest.

Another choice was to cut corporation tax – already the lowest in the G7 at 20%. Lower too than the 25% in China, and half the 40% rate in the United States.

That political choice will see our revenue intake from big business fall by £2.5 billion in 2020. That’s nearly twice the amount saved by cutting child tax credits beyond two children.

So closing the deficit and austerity are just the cover for the same old Conservative policies: run down public services, slash the welfare state, sell-off public assets and give tax cuts to the wealthiest.

This is why I stood in this race:

Because Labour shouldn’t be swallowing the story that austerity is anything other than a new facade for the same Tory plans.

We all want the deficit closed on the current budget, but there was no need to try to do it within an artificial five years or even the extra five years George Osborne mapped out two weeks ago.

If the deficit has been closed by 2020 and the economy is growing, then Labour should not run a current budget deficit – but we should borrow to invest in our future prosperity.

You don’t close the deficit fairly or sustainably through cuts.

You close it through growing a balanced and sustainable economy that works for all. And by asking those with income and wealth to spare to contribute more.

If Osborne’s forecasts are right there won’t be a deficit by 2020, but if – like last time – he is proved wrong and he only again manages to halve the deficit then I make this pledge:

Labour will close the current budget deficit through building a strong growing economy that works for all. We will not do it by increasing poverty.

The discussion about the deficit leads us to the clearest possible choice.

Rather than remove spending power from the economy and damage growth and future prosperity, Britain needs a publicly-led expansion and reconstruction of the economy.

We must put this centre-stage as the alternative to the current model of austerity for the poor, and deregulation, privatisation and never-ending corporate tax sweeteners for the super-rich and big business.

We need a fairer system for all, including on taxation..

But as a principle to create the kind of economy we need, Britain needs sharply rising levels of investment in the economy.

Faster growth and higher wages must be key to bringing down the deficit. Increased tax receipts and lower benefit demand are a better way forward than shutting local libraries and attacking the working poor.

If there are tough choices, we will always protect public services and support for the most vulnerable. Instead we will ask those who have been fortunate to contribute a little more. With a sustainable investment plan, we can ensure more people fall into that fortunate category too….

You cannot cut your way to prosperity. We need to invest in our future.

A strategic state cannot leave our infrastructure to deregulated privatised markets. They are failing people and holding backing our economy.

Modern housing, transport, digital and energy networks are the foundation stone of a modern economy, and we need to ensure they are among the best in the world.

Public investment in new publicly-owned infrastructure so that a future chancellor can deliver a sound economy, not just sound-bites….

The ‘rebalancing’ I have talked about here today means rebalancing away from finance towards the high-growth, sustainable sectors of the future. How do we do this?

One option would be for the Bank of England to be given a new mandate to upgrade our economy to invest in new large scale housing, energy, transport and digital projects:

Quantitative easing for people instead of banks….

But whatever tax laws we pass, we won’t get a progressive tax system in reality unless we can enforce it and collect the tax we are owed…

Therefore I am announcing today that my fairer tax policies will include:

- The introduction of a proper anti-avoidance rule into UK tax law.

- The aim of country-by-country reporting for multinational corporations.

- Reform of small business taxation to discourage avoidance and tackle tax evasion.

- Enforce proper regulation of companies in the UK to ensure that they file their accounts and tax returns and pay the taxes that they owe.

- Lastly, and most importantly, a reversal of the cuts to staff in HMRC…

[Our vision] means we judge our economy not by the presence of billionaires but by the absence of poverty; not only by whether GDP is rising, but by whether inequality is falling.

Labour must become the party of economic credibility AND economic justice.

Liz Kendall

On 30th June, Liz Kendall made a major speech at Reuters which centred on the economy, and was entitled “Responsibility and Reform”. The speech was set out in full in The Independent, and as with the other candidates, we recommend reading it in full. She said:

Today I’m here to talk about how Labour restores its economic credibility. How we become the responsible government this country needs – and the reforming government it deserves.

In today’s interdependent world much of our prosperity depends on the success of what happens beyond our borders. And the events in Greece, if allowed to spiral out of control, it will damage us here in the UK.

We need the Greek government and the Eurozone to find a mutually acceptable way forward. The Eurozone countries must seek every possible opportunity to secure a deal, so that Greece remains in a secure Eurozone. Similarly, the Greek government must make every effort to agree a timetable for structural economic reforms…

Over a century and a half, Reuters has had to innovate and adapt – embracing new technologies, entering new markets and always keeping an eye on the future.

I think we face similar challenges as a country. The world is changing fast and this can be an era of great opportunity for Britain. We have new technologies to work with, new partners to trade with and great national assets to build upon. We must be ready for the future.

That means fiscal responsibility, so that we spend less on debt interest and more on the things that we care about: creating prosperity and reducing inequality. And it means economic reform, so we spread power and see living standards rise when public finances are tight. Responsibility and reform.

The Government’s economic policy has failed on its own terms. George Osborne told us there would be no budget deficit by now, but we are not even close to wiping it out. He promised to rebalance the economy but we still face major problems in skills, productivity and the distribution of growth.

We won’t achieve sustained economic growth on the back of a property bubble. In parts of this city we have homes earning more than their owners. If we are not careful this will sow the seeds of the next financial crisis.

Under the Conservatives Britain has become world-class at creating low-paid jobs, and second class on the jobs of the future.

We have a Chancellor who talks about a ‘global race’ but an economy stuck in the slow lane. For the first time, the majority of people living in poverty are actually from working families. This is a national scandal, not an economic record to be proud of.

So it is Labour’s job to provide an alternative that people can believe in. That starts with re-establishing our reputation for fiscal responsibility.

The financial crisis came about because of deep-seated international problems in the financial system. The Tories would like to write this out of history but it is the truth.

It is also true that countries are not like households. Sometimes, in some years, governments need to run deficits. If Britain had not run a deficit at the start of the financial crisis the social and economic costs would have been much higher. But any country’s capacity to deal with shocks is dependent on long-term strength.

And long-term strength comes from only running deficits when you have to, bringing them down as soon as you responsibly can, and running surpluses in the good years. Because however much we tell the truth about the causes of the financial crisis, any political party that wants to be elected must be trusted with people’s money.

Labour does not have that trust – and this must change. People expect us to act responsibly because they know the damage that’s done when that doesn’t happen. People’s taxes spent on servicing our national debt, instead of funding public services. This isn’t just a waste – it’s also a risk.

Could the public finances withstand another crisis as deep as the last? No they could not. And as long as that is the case, our debts are too high. So under my leadership Labour will not take risks with our country’s future.

We will bring debt down as a proportion of our GDP and we’ll make surpluses in the good times. We’ll do this so that we are strong enough to withstand economic shocks. And so we spend less on debt interest payments and more on making this country richer and fairer.

Fiscal responsibility is part of a proud Labour tradition. People forget the strong commitment to fiscal responsibility in previous Labour governments.

In 1923 the manifesto of our first government demanded “the steady drain of a million pounds a day in interest is stopped”.

In his 1948 budget statement Stafford Cripps said: “We must secure an exceptionally large Budget surplus”.

In 1964 Harold Wilson’s election winning manifesto criticised “an ever-increasing burden of interest payments on the national debt, [while] vital community services have been starved of resources”.

And in 1997 Labour again won power because we were trusted on the public finances. In its early years the last Labour government delivered three budget surpluses in a row – more than the entire Thatcher-Major era delivered.

So when people say that fiscal responsibility is a Tory idea they are wrong. Worse, they are playing into our opponents’ hands.

Sound public finances are not an alternative to Labour values: they are Labour values. And they are the country’s values too. Remembering this is the first step we take in winning back the trust of the British people.

Balancing the books is not just about how much you spend, it’s also about how much you earn. That’s why we need economic reform alongside fiscal responsibility, so that living standards can rise and everyone can share in the country’s future success…

When too much power is centralised in Whitehall it holds us back. When power is centralised in markets the same is true. So just as we must reform the state to make it more responsive – we must reform markets to make them truly competitive.

This matters most in finance. We are strong in financial services but the sector should be there to serve the rest of the economy. Because finance drives investment, and investment drives productivity.

It’s what turns good ideas into commercial propositions. It’s what enables small companies to become larger and more productive. And it’s what equips domestic traders to become international exporters. But we have too little variety and too little competition in our banking sector….

Reform of our finance system is how we give businesses the power to invest and grow. The aim of this must never to be anti-bank – but to be aggressively and insistently pro-business.

Some reflections on what the candidates say

If one is to learn lessons, it is important to learn the right ones. If one is going to apologize for past errors, it is vital that the sole or principal error is correctly identified. All candidates accept that the electorate needs at least some suasion that a future Labour government will run the economy soundly and securely, since it is a fact that the financial crisis came about on its watch, with a bigger impact in the UK than in most countries. So to identify the causation of the crisis, and drawing the right lessons is of great importance.

All of the candidates seem to accept that the principal cause of the global financial crisis was not high public debt or spending as such, but most are vague as to what did cause it.

Yvette Cooper got somewhere close when she told the BBC back in May:

the real economic issue of the time was that we had banks who were involved in huge private lending that nobody had spotted the scale of; private sector debt that had been growing up that was unsecured; the links between the financial sector all over the world.

The problem here is that many (including of course PRIME’s director Ann Pettifor) had indeed “spotted” the scale of private debt building up and foresaw the crisis – so for the government and Opposition not to have seen it tells us a lot about a common blinkered view.

But at least Ms Cooper is clear on the cause. Since she became a candidate, she has not (to my knowledge) publicly addressed this issue of what caused the crash.

So what does Andy Burnham say about the financial crisis?

We achieved many great things but we can see now that it would have been better to have been spending less in the run-up to the crash. It wouldn’t have prevented it.

Our investments in public services didn’t cause the global financial crisis. But it would have meant we were in a stronger position to deal with the consequences.”

There is no explanation at all from him about the causes of the financial crash, it just happened, an Act of God! This is therefore worse than Yvette Cooper. Instead of assessing the degree of Labour government’s responsibility for the crash/crisis, through deregulation and failure to oversee the finance sector, he simply asserts that “we should have been spending less”, even though public debt as a percentage of GDP was not rising. This completely accepts the false “framing” of Mr Osborne.

Next, what does Liz Kendall tell us about the causes of the crash?

The financial crisis came about because of deep-seated international problems in the financial system. The Tories would like to write this out of history but it is the truth.

It is also true that countries are not like households. Sometimes, in some years, governments need to run deficits. If Britain had not run a deficit at the start of the financial crisis the social and economic costs would have been much higher. But any country’s capacity to deal with shocks is dependent on long-term strength.

And long-term strength comes from only running deficits when you have to, bringing them down as soon as you responsibly can, and running surpluses in the good years. Because however much we tell the truth about the causes of the financial crisis, any political party that wants to be elected must be trusted with people’s money.

This has the merit of referring to “problems in the financial system”, and indeed to “causes”, but in no way explains anything further, and fails to say what if any responsibility the Labour government (supported by the Conservatives) had for it. The implicit message is that pre-crisis deficits were a major contributory factor.

There is a deep lack of logic to all this. If the finance sector had not blown up, there would have been no problem with the public finances – or with Labour’s reputation! But it did blow up – affecting countries with right-wing and social democrat governments alike. Not due to public debt but because of private debt and the excesses of the private finance sector. Governments (of various hues) had a total blind spot for this – to prevent it would have meant challenging the basic premise of financialised globalisation which they had all taken for granted.

None of the three “mainstream” candidates have accepted any degree of Labour (and Conservative) responsibility for the true failure; they have rather accepted all or much of Mr Osborne’s false framing of the problem as one of public debt and public finances.

Finally on this point, Jeremy Corbyn:

…and secondly the economic reality that it was the reckless behaviour of the finance sector that got us into this mess and they should be paying for it.

If we cast our minds back almost eight years, to September 2007, customers were not queuing out of the doors of Northern Rock branches because a Labour government had spent too much on nurses and teachers. Just two weeks before, George Osborne had backed Labour’s spending plans.

Labour does have some responsibility for the crash. Not because we spent too much, but because we didn’t regulate enough.

Whether or not you favour his programme and candidacy as a whole, it seems to me undeniable that on this crucial point, Mr Corbyn is right. It was not Labour overspending or fiscal irresponsibility that caused the crash or made it materially worse – but the last Labour government (together with all its peers, and with the Opposition) was partly responsible for it due to its failure to regulate the finance sector properly and restrain the massive build-up of private debt across both financial and non-financial sectors.

Are deficits a problem?

The assumption shared by all candidates – except to some extent Mr Corbyn – is that good husbandry requires governments to avoid deficits, save maybe in very difficult times. The duty in normal times, we infer, is to run a budget surplus and use it to “pay down the debt”.

We need to consider the different types of deficit (I ignore alleged “structural deficits” for now). Deficits can be considered in cash terms – how much have we borrowed? In which case the deficit may go up from year to year – even if as a percentage of national income it comes down.

Or we can look at deficits as a percentage of national income (GDP) – and here it is the size of the “cake” of economic activity that in particular matters – if each year the “cake” increases by a greater percentage than the (cash) budget deficit rises (if it does rise), then the deficit as a percentage of GDP falls – without cutting public expenditure.

This point is vital, since it has been the way that the UK – under Conservative and Labour governments – has for over 50 years succeeded (for the most part) in reducing or keeping down the debt to GDP ratio.

It has been rare indeed NOT to run an overall budget deficit. Since 1960, there have been just 9 years out of 55 when the UK has had a budget surplus or deficit of less than 1% of GDP. Of the 7 years when an actual overall surplus was achieved, four were under Labour governments, 3 under Conservative governments.

The distinction between current and overall deficits

This brings us to the second distinction to be made over “deficits” – between an overall deficit, and a current budget deficit. The last paragraph and its statistics refer to overall deficits – i.e. overall net borrowing. That includes borrowing in respect of capital (investment) expenditure as well as (if necessary) in relation to current spending. (Annual investment spending has normally ranged between 1.5% and 3% of GDP)

As Liz Kendall rightly commented, “countries are not like households” – but it is worth recalling that even households do tend to borrow long-term for major long-term investment purposes, e.g. house purchases or major improvements.

The candidates are again unclear on whether borrowing for capital purposes comes with their definition of “deficit” (we assume yes unless they tell us otherwise) – or whether they are only referring to avoiding any current budget deficit.

If the latter, then it is generally impossible to achieve an overall surplus that enables a government to “pay down the debt”, since if one borrows for capital purposes, any surplus on current account will be used to pay for part of the capital programme, not for reducing overall debt.

Again, Jeremy Corbyn is clear on the difference, when he says:

We all want the deficit closed on the current budget, but there was no need to try to do it within an artificial five years…”

Yvette Cooper referred to the current deficit when speaking to the BBC before announcing her candidacy (“The deficit at the time was 0.6%, the current deficit…”), but her speeches since do not clarify her view on the distinction.

Liz Kendall made this commitment:

We will bring debt down as a proportion of our GDP and we’ll make surpluses in the good times.

…only running deficits when you have to, bringing them down as soon as you responsibly can, and running surpluses in the good years.

This leaves unclear what she means by the term “deficit”, and whether in ordinary times (neither “good” nor “dreadful”) an overall (not current) deficit is acceptable provided that it still leads to the debt/GDP ratio falling. This is of course difficult stuff to get across to the wider public, but we really need to know what the candidates mean

Andy Burnham is also opaque – he promises

Labour under my leadership will always run sound public finances and we will reduce the national debt, back toward its sustainable pre-global financial crisis levels.

But it is possible to borrow for investment purposes and still reduce the national debt if by that we understand – as the final clause possibly implies – that he means the pre-crisis level as a percentage of GDP.

Jeremy Corbyn accepts the desirability of getting rid of a current budget deficit (if achieved by increased economic activity) and appears to accept that borrowing for investment is acceptable for him:

if the deficit has been closed by 2020 and the economy is growing, then Labour should not run a current budget deficit – but we should borrow to invest in our future prosperity. You don’t close the deficit fairly or sustainably through cuts.

In brief, my conclusion is that on the issues of basic macroeconomic and fiscal policy, Jeremy Corbyn has, to his credit, expressed the clearest and (macroeconomically) soundest view on the role and acceptability of deficits, and on the distinction between borrowing for current purposes, and for investment purposes. He is also clearer than the others on the need to reduce the deficit by economic activity, not further cuts.

Where however I have problems with the current formulation of his policy is around the (to me) excessive role and prominence given to taxation as the principal – certainly by far the most detailed – policy tool. A fair redistributive tax system – in which tax evasion and avoidance are clamped down on – is vital, and far more than the other candidates, he does underline the role of tax as an issue in economic justice. This is absolutely right.

But he dedicates much more space to tax than other issues (such as types of investment and how to raise levels of economic activity), and goes on to argue:

The biggest issue facing British politics right now is not whether the top rate of tax should be 45% or 50%, or whether corporation tax should be 18% or 20%. The big question is how to get some of the wealthiest individuals and biggest corporations to pay anything like their fair share.

A big question, yes. The big question, or the biggest question – well, in my view probably not. The electorate need a more positive vision of our economic and social future – and how to create tomorrow’s economy than comes across thus far.

Silly and wrong to fall for Mr Osborne’s economic framing

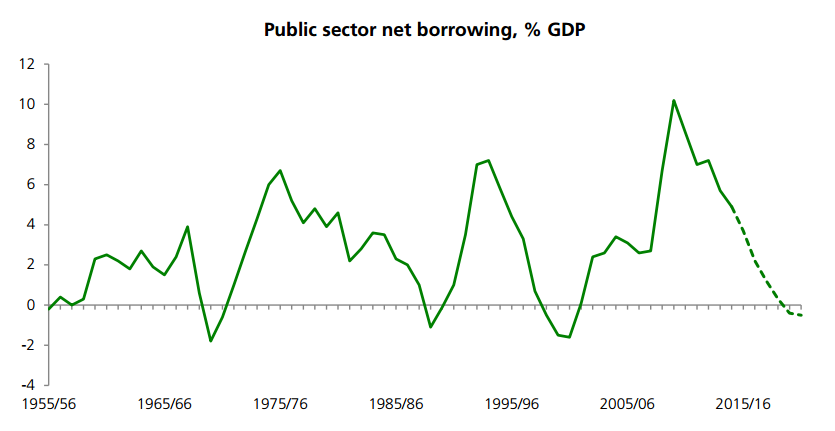

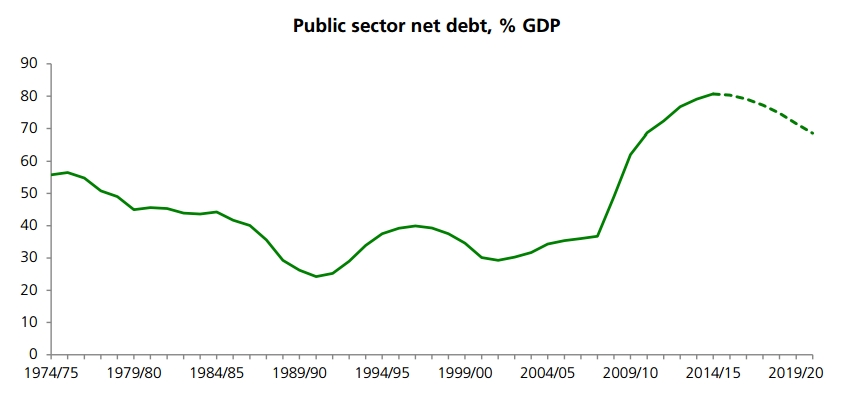

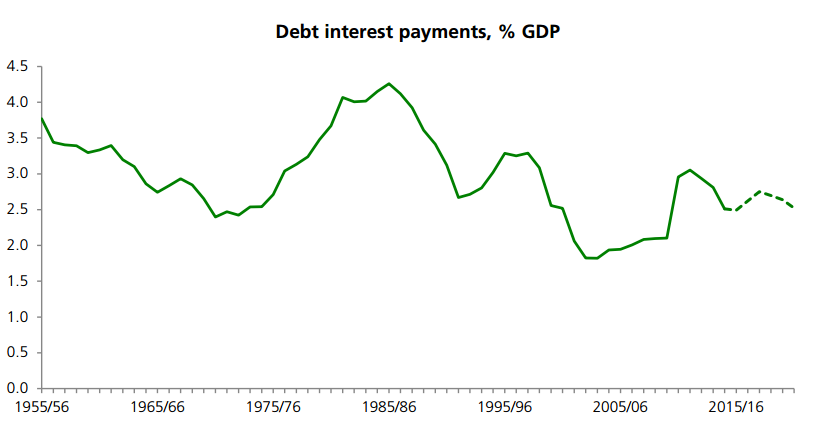

Final point to conclude this overlong blog – I offer the following three charts, which I hope clarify or demonstrate many of the points raised above. All three come from a really useful short House of Commons Briefing Paper by Matthew Keep, dated 28 July 2015.

The first chart deals with net borrowing as a percentage of GDP (i.e. the overall deficit), the second with public sector net debt as a percentage of GDP, and the third with debt interest payments as a percentage of GDP.

You will see that prior to the financial crisis, deficits were not historically high, that public sector debt was relatively low and stable, and that debt interest payments are also relatively low in historical terms. (All as % of GDP, which is the best way to look at them). So to fall for Mr Osborne’s economic framing is both silly and wrong.

3 responses

Jeremy why no reference to the alternative perspectives of Abba Lerner’s "Functional Finance" and Wynne Godley’s "Sectoral Balances Accounting" which are merged into Modern Monetary Theory?

From selling Gold reserves to ruinous PFI we see the wholesale waste of 10s of Billions. Acts so ridiculous that surely they have to denounce in Old Soviet style their economic incompetents [Brown, Balls & Darling] or if they consider it malicious demand a police investigation. Point is Labour were incompetent even if Osborne supported their incompetence and overall %tages of debt within historical norms.. They turned the Public finances into a huge subsidy spigot for the financial industry and indeed many other industries for seeming no competent reason.

The Financial Crisis of 2008 agreed they are not responsible for per se. Nonetheless the cavalier handing over of state income to friends in return for poorer services is a crime that is under mentioned Serco A4E G4S etc.

Labour were profligate and incompetent just as Osborne is. The next crisis we might find out just how many loans are guaranteed by the state now which I believe will be the next under reported fraud debt…

Bit one-eyed, methinks.