The latest GDP figures for Greece, relating to Q4 of 2016, are disastrous. For Greece first and foremost, but also for the credibility of the EU and IMF’s failed harsh austerity (but on the EU side no-debt-cancellation) policy. Far from evidencing the long-promised recovery, they show a new decline in GDP – both on the previous quarter (after seasonal adjustment) and year on year.

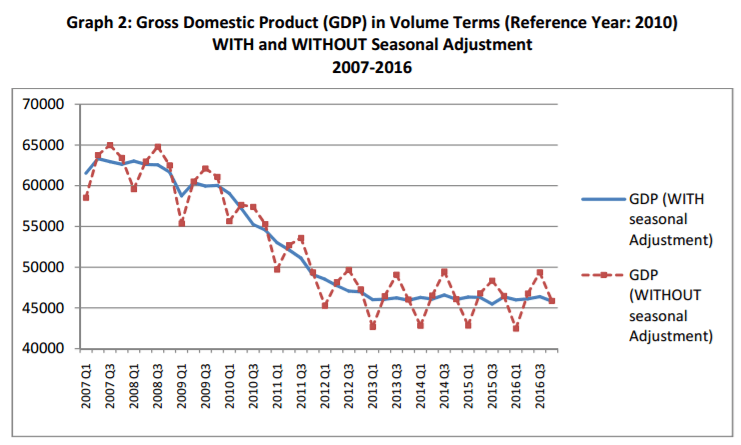

In fact, the economy has been broadly stagnant at a low level since 2013. In constant volume terms, GDP fell by over 27% from (peak) Q2 2007 to Q4 2013, and in Q4 2016 it was 0.3% smaller than in Q4 2013. In Q4 it was only marginally higher than the post-crisis record low to date, Q3 2015.

This chart from Elstat (the Greek Statistical Office) shows the development of GDP over the last decade:

Chart from Elstat

What is more extraordinary is that current price (i.e. nominal) GDP has fallen even further than real GDP over the decade – by 28.5% From 2008 to 2016, GDP fell quarter-on-quarter in no fewer than 27 out of 36 quarters, of which two in 2016.

Looking at the elements of GDP, we see that nominal consumption expenditure in Q4 was almost identical to the year before, with household consumption up a fraction, and government “consumption” down by about the same. The significant fall was in GFCF – capital investment – down 18%. Net trade improved slightly on Q4 2015 as exports increased more than imports – but exports were lower than in Q4 2014, so there has been no big turnaround in trade.

Turning to income, there has been scarcely any movements over the last two years in Q4. The figure for compensation of employees is almost identical to that of 2015 and 2014, meaning that the small increase in employment is offset by lower wages. The gross operating surplus / mixed income figure is similar to Q4 2014, but a little higher than 2015.

The general picture of stagnation at a level far, far away from a positive equilibrium is emphasized when we look at the employment and unemployment statistics, also via Elstat:

Chart via Elstat