On 8th July Greece applied to the European Stability Mechanism (ESM) for financial support in the form of a loan, for a 3 year period to 2018, “to meet Greece’s debt obligations and to ensure stability of the financial system.” On the same day, Jeroen Dijsselbloem, Chairperson of the ESM Board of Governors, wrote to the Governor of the ECB and the EU Commissioner for Economic and Financial Affairs. Greece’s fate as member of the Eurozone would appear to hang on the outcome.

In this letter, Mr Dijsselbloem (who also chairs the finance ministers’ Eurogroup) said:

I hereby entrust, in my capacity as Chairperson of the ESM Board of Governors, the European Commission, in liaison with the European Central Bank, with the following tasks:

(a) to assess the existence of a risk to the financial stability of the euro area as a whole or of its Member States;

(b) to assess, together with the International Monetary Fund, whether public debt of the Hellenic Republic is sustainable; and

(c) to assess the actual or potential financing needs of the Hellenic Republic.

This formulation is necessary to comply with the legal requirements of the ESM Treaty of 2012, ratified by all Eurozone countries. Any financial support is to be granted “On the basis of the request of the ESM Member and the [debt sustainability] assessment…”.

The ESM is in legal form a separate international legal entity, set up precisely to get round the EU Treaties which (foolishly) forbid the provision of credit facilities to governments and public bodies by the EU or other Member States.

The involvement of the IMF, under (b) above, is said in the Treaty to be “where appropriate and possible” – one presumes that this condition will be met despite recent differences!

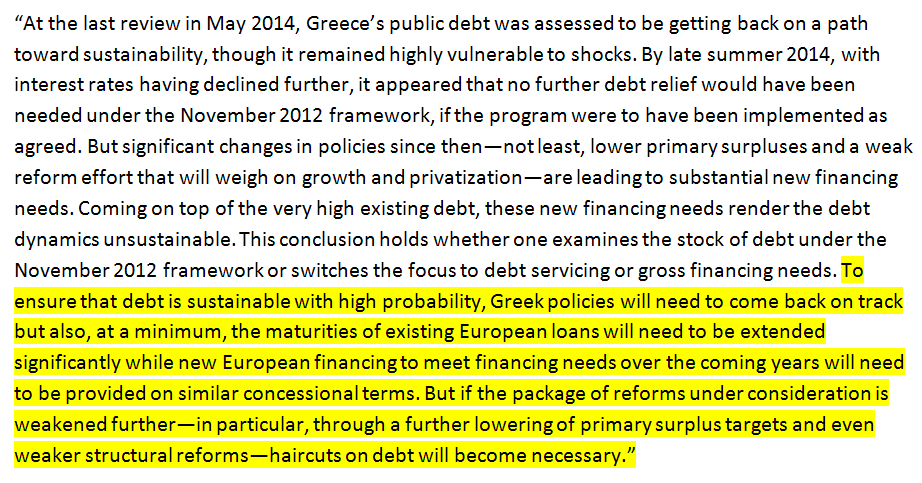

For the IMF have, you will recall, recently called into question the sustainability of Greece’s debt held mainly under the terms of the (expired 30th June) EFSF loan. Here is the summary of the “Greece: Debt Sustainability Analysis Preliminary Draft” issued on 26th June (our highlight):

So “at a minimum, the maturities of existing loans will need to be extended significantly”, and if primary surplus targets are lowered (i.e. the pace of austerity slowed), “haircuts on debt will become necessary”.

The draft report goes on to say (p.3):

“However, very significant changes in policies and in the outlook since early this year have resulted in a substantial increase in financing needs. Altogether, under the package proposed by the institutions to the Greek authorities, these needs are projected to reach about €50 billion from October 2015 to end 2018, requiring new European money of at least €36 billion over the three-year period ”.

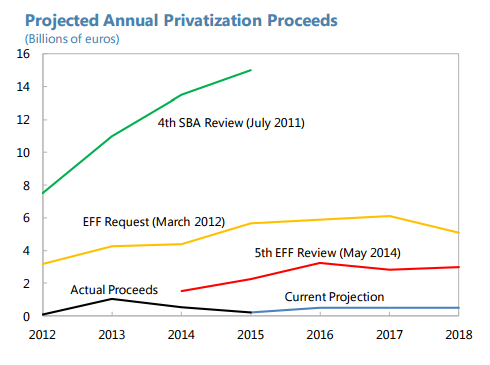

The reference to “since early this year” is unfair to the new incoming government, in that much of the problem dates back to previous governments. For example, the hopelessly optimistic anticipated proceeds from privatisation have been consistently downgraded, as this chart from the IMF draft report demonstrates:

Moreover, while real GDP in Greece did marginally increase in 2014 over 2013, already by Q4 it had slowed right down, and employment had stopped growing. In particular – as it affects the debt to GDP ratio – nominal GDP continued to fall during the year, and the country remained in deflation. So Syriza inherited a disastrous situation from New Democracy, and the EFSF Greece programme of 2012 was already failing.

The recent propaganda that Greece was on the verge of major growth and recovery, stopped in its track by the incoming government, is simply… propaganda.

But which way forward?

If the draft IMF report is finalised as it stands, it appears that on the basis of the terms imposed (agreed) to date, the debt is not presently sustainable, but could be made so by extending maturities and adding new financing. But events of the last few days – with the ECB in effect forcing capital controls by blocking any extension to its Emergency Liquidity Assistance – are likely to have worsened Greece’s financial position beyond that so far taken into account. So the support would need to be greater.

This then becomes an existential choice for the eurozone governments – to offer significant new support, or to refuse and leave Greece in a position in which it cannot and will not be able to service or repay much of its debt, most of which is owed to the Eurozone governments or their financing “vehicles”. Germany and France between them are owed around €100 billion.

It is of course conceivable that the IMF Executive Board will not approve the findings of the draft report, though it seems hard to believe it will find it to be less unsustainable than the draft, and the decision to publish the draft is itself a powerful “statement”.

The only alternative – either by political choice, or if the debt is assessed as unsustainable on any reasonable showing – is the lose-lose scenario apparently favoured by many in the German government and establishment, including Finance Minister Schäuble and Bundesbank President Weidmann. Under this scenario, no more support is given. Greece then – in practical (if not legal) terms – exits the eurozone and is left to its own monetary and fiscal devices, de facto but not de jure bankrupt (alas, there is no legal bankruptcy or insolvency process for sovereigns). No doubt it would try to repay the IMF as and when possible, but its European partners would lose out still more.

Perhaps then the creditors’ best option would be to sell their Greek debt to Paul Singer and his Elliott Management vulture funds for 20 centimes in the Euro. (1)

(1) Paul Singer is the US Republican billionaire whose companies (based in tax havens) buy up “junk” government debt from bond-holders and uses every known legal process to force payment of 100% of the face value of the bonds plus compound interest. He has been pursuing Argentina for over a decade, with the unjust assistance of the US court system, as we have set out here and many other times. Operators such as his are known as “vulture funds”.