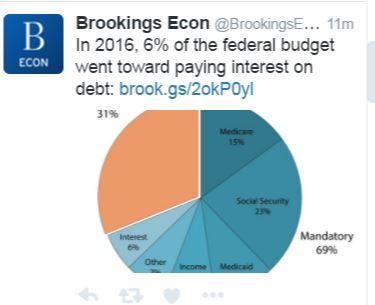

I was looking at my Tweetdeck this morning when I came across this tweet from the Brookings Institution:

Now it is clearly a Good Thing in principle for the US Federal government’s budget to be explained in clear and simple ways, but why – I asked myself – do Brookings choose to concentrate today on interest payments (which form just 6% of outlays) rather than the programs that President Trump wants to cut to shreds? I clicked on the link and found this in their explainer:

“WHY DO WE SPEND SO MUCH ON INTEREST?

The government has borrowed a lot: The federal debt held by the public amounted to slightly over $14 trillion by the end of 2016, a sum equivalent to roughly 77 percent of the U.S. economy. This level of debt is very high by historical standards. The only previous experience with debt this high was at the end of World War II. As a result, a sizable part of the budget goes to pay interest on that debt—in 2016, interest consumed a little over 6 percent of all federal spending. This is more than what the federal government spent on unemployment benefits, higher education, food and nutrition assistance programs, and pollution control taken together.”

The last sentence may be arithmetically true, but clearly serves another purpose – to make the reader think that government debt and interest payments are a growing problem, “crowding out” other – more beneficial – spending. The Trump White House makes this argument explicit in its recent draft 2018 budget plan:

“When debt levels keep increasing, more and more of the Nation’s resources are required to service that debt and are diverted away from Government services that citizens depend on. To help correct this and reach our budget goal in 10 years, the Budget includes $3.6 trillion in spending reductions over 10 years, the most ever proposed by any President in a Budget.” (My emphasis)

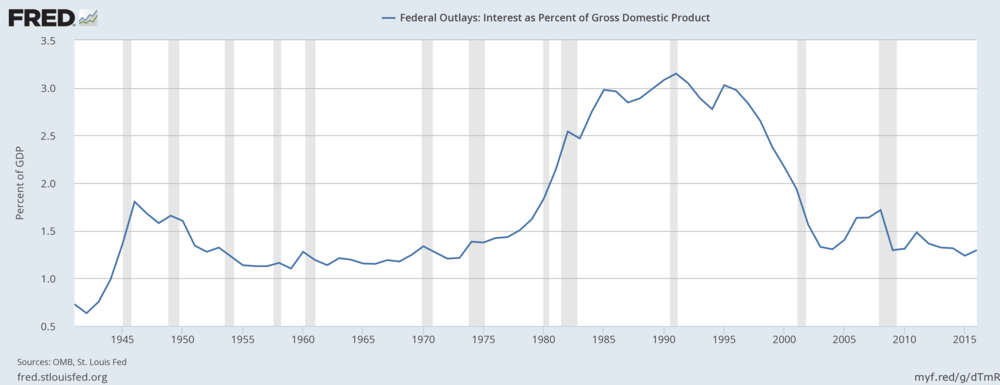

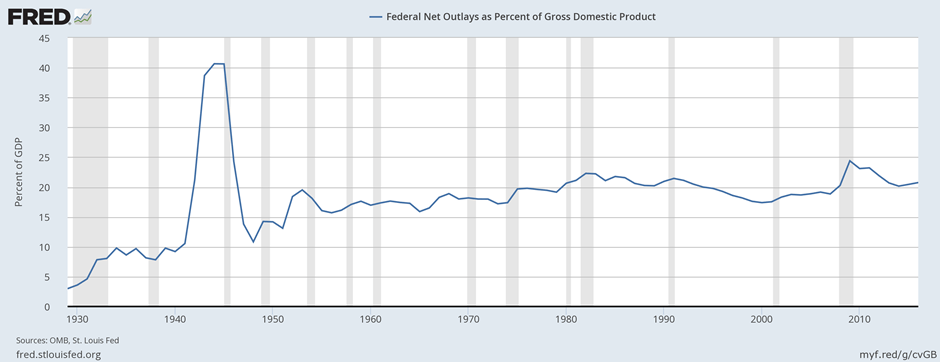

What the Brookings explainer fails to mention – and the Trump administration wish zealously to hide – is that Federal government interest payments as a percentage of GDP are no higher than they were in the 1960s and 1970s – and far lower than in the 1980s and early 1990s. They are only a tad above the Eisenhower mid-1950s level! This chart from the St Louis Fed shows it clearly:

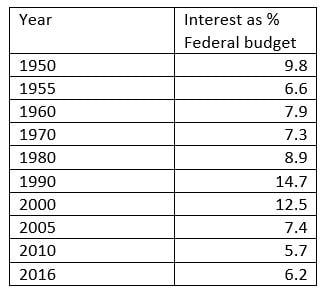

What is more, the percentage share of interest payments in the Federal budget is also close to a post-1945 low (table compiled by author from USgovernmentspending.com):

Source: http://www.usgovernmentspending.com/year_spending_2016USfn_18fs2n#usgs302

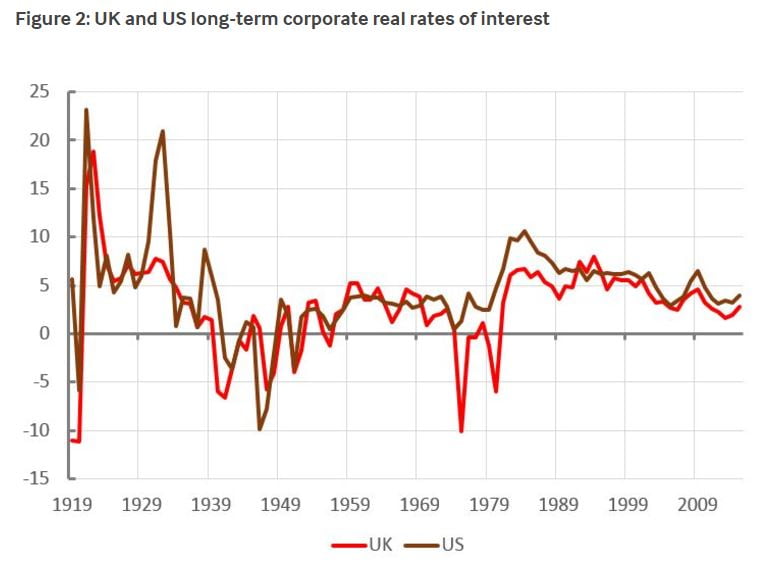

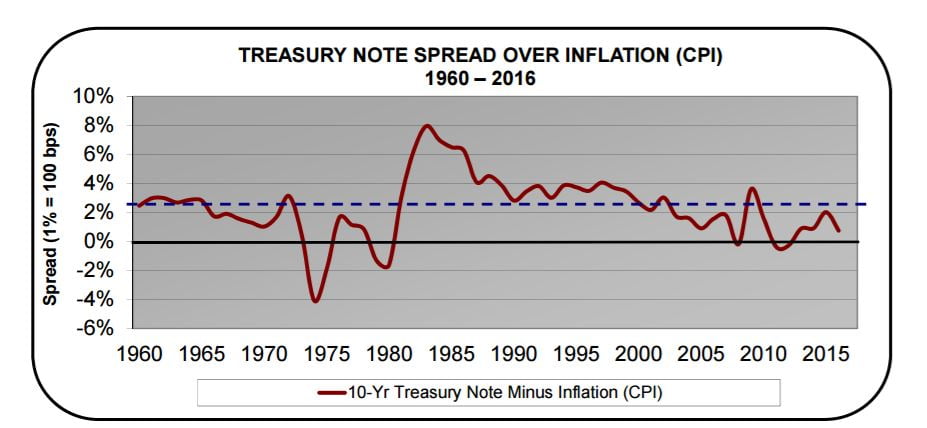

That is to say, interest payments as a share of GDP, but also as a share of the Federal government budget, rose greatly under President Reagan’s administration. As Geoff Tily has shown in his PRIME series on interest rates, the 1980s was a time when real interest rates (i.e. the nominal rate less annual inflation rate) rose to levels not seen since the Great Depression post-1929 – neoliberalism unleashed!

US Treasuries followed a similar path:

Source: Crestmont Research

And just in case it helps, Federal spending as a percentage of GDP was generally as high or higher under Presidents Reagan and Bush senior as it was in 2016!

Source: https://fred.stlouisfed.org/series/FYOIGDA188S

Brookings is not on the far libertarian right of US economic think-tanks, but is rather the High Established Church for financial globalisation. (Its President, Strobe Talbott, wrote in 1992 that “In the next century, nations as we know it will be obsolete; all states will recognize a single, global authority.” 25 years on, this is not looking a good call – instead, financial globalisation is endowing us with a bunch of Trumps, crooks and autocrats – not necessarily separate categories).

Brookings’ Board of Trustees is jam-packed with representatives of giant global hedge funds, banks (Deutsche, Goldman Sachs..) and ‘consultancies’ (McKinsey). They benefited from the high real rates of the 1980s and 90s, and have benefited ‘hugely’ from QE, despite/due to the low interest rates required after the crisis. They are likely to have a very ambiguous attitude to the Trump economic agenda, wanting the tax cuts and (if ever..) infrastructure investment, but alarmed at other policies as well as the chaotic policy contradictions.

The Brookings’ arm that produces the fiscal “explainers” is called the Hutchins Center on Fiscal and Monetary Policy; its Advisory Council’s co-chairs are Greg Mankiw (who chaired Bush junior’s Council of Economic Advisors) and Larry Summers, with Ben Bernanke among the advisers.

Two years ago the Center’s director David Wessel (a long-time writer for the Wall Street Journal) wrote this in another “explainer” – and nothing has materially changed since:

“The U.S. government is able to borrow at very low interest rates on global financial markets, and there doesn’t appear to be much private-sector borrowing that is crowded out by U.S. Treasury borrowing right now.”

The US Federal Reserve, we should also remember, has a triple, not a double mandate for monetary policy:

“The Federal Reserve Act states that the Board of Governors and the FOMC should conduct monetary policy ‘so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.'” (My emphasis)

(Maybe trustee Ben Bernanke can advise…)

Brookings and its Hutchins Center really should do better than focus on debt interest payments (which are stable) at the very moment when when President Trump is trying to slash every Federal budget head that contributes towards a civilised society. It is that budget, and its harsh impact and social consequences, that would be most likely to lead to fiscal problems downstream.