Sterling & Brexit: the Disaster Hypothesis

Many, and especially Brexit opponents, point to the sharp depreciation of sterling as evidence of imminent economic turmoil leading to disaster. For some depreciation itself is disaster, “The pound is the share price of UK plc,” according to David Blanchflower, former member of the Bank of England Monetary Policy Committee.

More analytical than this rather mercantilist “strong currency equals strong country” syllogism or anxieties over more expensive holidays are fears of the impact of sterling depreciation on employment and living standards, made by the distinguished economist Robert Skidelsky, as well as sometime sterling speculator George Soros.

How sterling depreciation affects employment and living standards cannot be predicted with certainty because of the complex relationship between exchange rates and the aggregate economy. The high anxiety over these and other economic consequences comes from the perceived severity of the drop in sterling exchange rates since the 23 June referendum and the presumption that Brexit was the main if not the sole cause.

ABCs of Exchange Rate Adjustment

During the postwar era of fixed exchange rates, 1945-1971 (so-called Bretton Woods system), regulatory policies severely restricted international capital flows. In Britain restrictions on the inflow and outflow of funds continued until their abrupt elimination by the Thatcher government in late 1979.

In that by-gone era budding economists learned in their classrooms that the balance of trade flows governed exchange rates. The story was a simple one. When country A imported more than it exported, its national currency accumulated abroad. The holders of the idle currency of country A would exchange it for their own national currency creating downward pressure on the exchange rates of country A. The government of country A could prevent depreciation of its currency by using its foreign reserves (i.e. US dollars) to buy back its own currency. If the trade deficit persisted, the government of country A would deplete its reserves and have no choice but to devalue (an administrative measure by a government, while depreciation refers to a market adjustment).

In the Bretton Woods era it could be argued that a “strong currency” indicated a “strong economy”. An export surplus would mean accumulation of foreign reserves and signal pressure for appreciation or revaluation (“strengthening” of the currency). The presumption that a trade surplus came from greater efficiency in national production completed the argument:

strong economy leads to strong currency

National efficiency → trade surplus → currency appreciation

The post-war appreciation of the Japanese Yen was frequently cited as the outstanding example of this argument in operation, though causality ran the other way, from a managed exchange rate and industrial policy to a stronger economy (see chronology of Japanese policy).

Whatever might have been the causality between national economic performance and national currencies in the postwar years, for the last three decades (going on four) trade flows have not determined the movement of exchange rates in the major countries. In the wake of eliminating exchange regulations, capital flows are the overwhelming determinant of international currency movements.

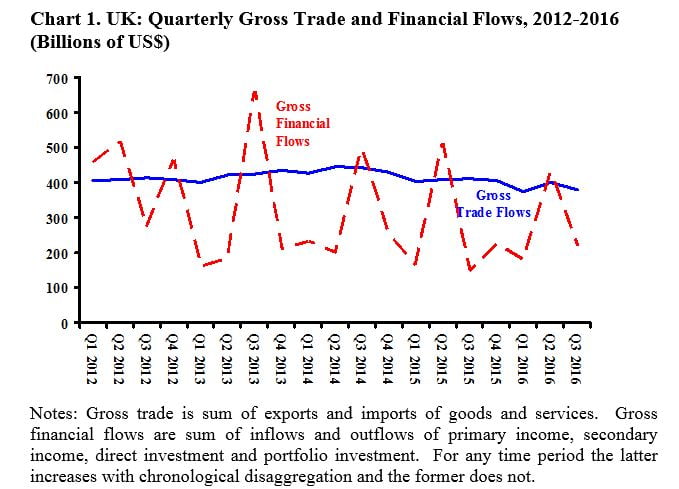

For no country does this generalization apply more than Britain, where the City serves as a global conduit for financial flows. The chart below partially indicates the extent to which financial flows dominate the British balance of payments and, therefore, movements in the exchange rate. The difference between net and gross is essential to understanding the impact of financial flows (see link in Chart 1 to Bank of England explanatory web page).

Every day in Britain money flows in and out of the City. The daily net flow understates financial movements and the longer the time period the more misleading is the net measure. For example, in 2015 net money movement in and out of Britain was minus US$79 billion while gross movements measured quarterly summed to over US$ one trillion (inflows and outflows added together rather than subtracted). Net financial flow or any time period short or long is only a statistic; the flows themselves influence exchange rates.

The enormous difference between net and gross only hints at the size and impact of capital flows, for it would increase arithmetically if we summed across months or days. The same is not true for trade flows, which involve an activity in form of a physical commodity or payment for a one-off service. Except for the category of “re-exports”, small for all major countries, there is no difference between net and gross exports or imports.

In Chart 1 the blue line shows total trade in goods and services (exports plus imports), measured in US dollars (as done in the source table). The currency movements associated with gross flows of goods and services are very stable. The quarterly average is US$413 billion and the standard deviation only 19 billion. By contrast, gross financial flows (the dashed red line) show great volatility, averaging US$314 billion across quarters with a standard deviation of 159 billion. Were statistics readily available by month they would probably show that financial flows far exceed trade flows.

Because currency flows consist of a stable component and a variable one, the latter will determine movements (an obvious inference validated by taking the first difference or differential). The temptation should be resisted to assign movements in the pound to volatile capital flows and the average level of the pound to relatively stable trade. The interactive relationship among the three, money flows, trade and the sterling rate, is far more complex. In my opinion the most likely causality is that financial flows determine short term exchange rates and short term exchange rates are one of many influences on trade flows.

Source: IMF and Bank of England (definitions).

Sterling Exchange Rates: 4 Decade Perspective

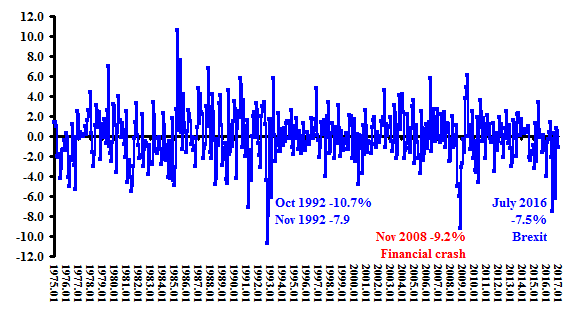

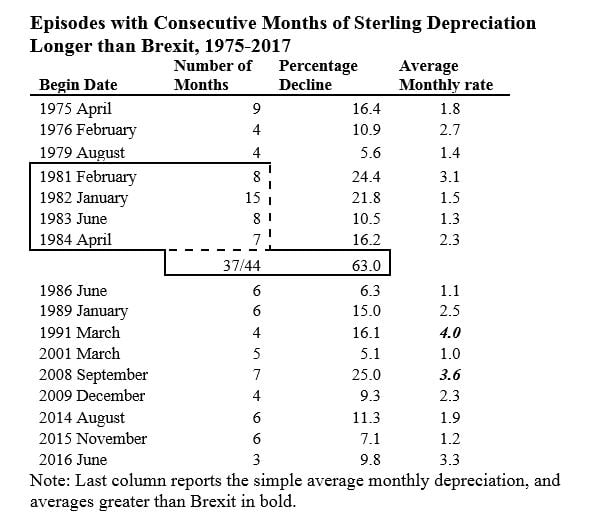

Having established the context for analysis, I turn to inspection of movements in the pound exchange rate over several decades. This inspection suggests that the fall in sterling since the referendum was not as extreme as some have suggested and not without precedent during the era of flexible exchange rates.

The Bretton Woods system in which governments pegged their exchange rates to the US dollar (itself linked to gold) ended in the early 1970s. After experiments with other mechanisms for fixing rates, most of the non-socialist countries adopted so-called flexible exchange rates.

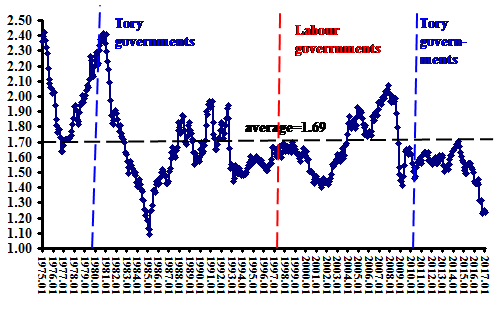

Chart 2 shows the US dollar to sterling exchange rate during the forty-two years of “floating” rates. The chart suggests that the two periods of Conservative government coincided with depreciations of the pound (“weakening”), while the Callaghan and Blair years coincided with appreciation.

The policy induced recession of the early 1980s resulted in a five year decline in the dollar-pound rate to near parity in February 1985. After a rise to almost US$1.90 in May 1990 four years of instability followed. This instability was punctuated by the pound dropping out of the exchange rate mechanism in September 1992. Most commentators attributed the recovery from the deep recession of the early 1990s in part to the sharp fall in sterling during 1992-93.

In the era of flexible exchange rates the longest period of pound appreciation occurred during 2001-2007 (with a brief drop in 2005). As during previous recessions the Global Financial Crisis brought a sudden and severe decline in sterling, though far less than in the Thatcher years. The latest bout of depreciation began not with Brexit but in August 2014, 16 months before Parliament passed the enabling bill for the referendum.

Chart 2. Monthly US Dollar to Sterling rate, January 1975 – January 2016

Source: Bank of England