pressandjournal.co.uk

“The country has to live within its means” – David Cameron, Prime Minister’s Questions, in response to the Leader of the Opposition, 16 September 2015

If there is one thing that unites Members of Parliament of left, centre and right, it appears to be a strange religious faith in the dogma, “we must eliminate the deficit and live within our means”.

In a current article in Socialist Economic Bulletin, John Ross writes:

John McDonnell, the new Shadow Chancellor, has created something of a stir by his firm opposition to budget deficits to cover current expenditure – writing ‘let me make it absolutely clear that Labour under Jeremy Corbyn is committed to eliminating the deficit and creating an economy in which we live within our means.’

The so called ‘Keynesian’ left has attempted to make a point of defending budget deficits, presenting this as a hallmark of the left. These latter views are politically damaging because they are economically false. Neither do they derive from Keynes but from the confused views of academic pro-capitalist economics. John McDonnell is entirely correct on this point to oppose borrowing to cover current expenditure over the course of the business cycle. [our emphasis].

John Ross suggests here that John McDonnell was referring only to a current budget deficit expenditure (i.e. not including capital investment). This was far from explicit in the original Guardian article:

[D]eficit denial is a non-starter for anyone to have any economic credibility with the electorate. This was a key finding of the poll recently published by Jon Cruddas, examining why Labour lost the election.

So let me make it absolutely clear that Labour under Jeremy Corbyn is committed to eliminating the deficit and creating an economy in which we live within our means.”

In his “Economy in 2020” paper, Corbyn himself had put the matter quite differently, and in our view more sensibly:

We all want the deficit closed on the current budget, but there was no need to try to do it within an artificial five years or even the extra five years George Osborne mapped out two weeks ago.

If the deficit has been closed by 2020 and the economy is growing, then Labour should not run a current budget deficit – but we should borrow to invest in our future prosperity.

You don’t close the deficit fairly or sustainably through cuts.

You close it through growing a balanced and sustainable economy that works for all. And by asking those with income and wealth to spare to contribute more.”

Following his diatribe against “the so called ‘Keynesian’ left”, John Ross prays in aid an earlier article in which he criticises the traditional GDP formula:

Y = C + I + G + NX

where Y is GDP, C is consumption, I is investment, G is government and NX is net exports.

To simplify, he proposes that C + I + G should be replaced by C(p) + C(g) + I(p) + I(g)

This formulation separates the government (g) contribution into two categories – government consumption and to investment, rather than lumping all of government expenditure into one.

On this formulation, we agree with John fully. This is a more helpful way of analysing the respective contributions to GDP. He goes on, however:

A key reason the lack of clarity created by introducing the confused term G is practically economically significant is the consequence for the structure of the economy when is there is unspent private saving, including non-invested company saving – i.e. private saving is not being transformed into private investment, and the government steps in to maintain demand.

The government may either increase “consumption”, or it may increase “investment”. This matters, because, John writes:

capital investment is the quantitatively most important factor in economic growth. Therefore reducing the proportion of the economy used for investment, other things being equal, will reduce the economic growth rate.

Both economic theory and practical results show that in a capitalist economy, not necessarily an economy such as China’s, there is greater resistance to government spending on investment than on consumption – as state investment involves an incursion into the means of production, which in a capitalist economy by definition must be predominantly privately owned. This theoretical point is confirmed by the fact that state expenditure on consumption has historically risen as a proportion of GDP in most capitalist economies since the economic period following World War II while state expenditure on investment has in general fallen in the same period.

The acceptance of government expansion of consumption, but opposition to government investment, therefore has the consequence that when so called ‘Keynesian’ methods of running government budget deficits are used, and G rises, what in practice happens is that C(g) rises but I(g) does not.”

This rise in government consumption, he says, has the effect of reducing investment, and thus reducing the economic growth rate. [1]

It is true that, in a crisis, government investment spending is considered easier to cut back, but that is not mainly for the reasons given. It is far easier to cut a programme that has not yet started, or to freeze new school buildings etc., than it is to dismiss many thousands of employees. While there is indeed strong and unjustified resistance to government investment that “involves an incursion into the means of production” (including the cries of outrage and horror at any even minor proposals for public ownership of natural monopolies), most government investment positively helps the private sector, in two ways.

First, by improving the common public infrastructure, and second, because most of the actual construction work is – though publicly funded – carried out by the private sector. Thus a new NHS hospital is (or should be) a public asset, but the building firm will surely be a private one. This is why there is in fact – in many areas – no contradiction between the interests of society, and of sections of the private sector (and their employees). This should be a selling point for public investment!

Moreover, government “consumption” in most respects does not have the same social character as private consumption, and it is a mistake to confuse them. Current government spending, i.e. the budget on which deficits are calculated, is made up (1) of government (including local government) spending programmes on all the major services, and (2) of “transfer payments”, such as pensions and other benefits. Much of the progressive increase in socially useful government consumption is, to most citizens, a positive and necessary thing – on hospitals, education etc. It includes of course “bad stuff” like current budget spending on maintenance of Trident, but decisions on current spending are (or should be) the stuff of democratic decision-making.

If government ceases to provide a service (thus reducing government consumption), those who need it go without or must pay for it in the private sector. In areas like health, this means greater private savings (as people prepare for bad times), which are then available for private (good or bad) investment – but have the effect of deferring private consumption overall as well.

This is perhaps most striking in China. There, the state does not yet provide an adequate safety net of public services for all citizens, i.e. the state does not “consume” enough which means citizens are obliged to save more for ill-health, old age etc. This is to the detriment in particular of rural migrants to the city who under the hukou system remain registered in their area of origin, and are not entitled to all the public services available to city-registered residents. Chinese Premier Li Keqiang fully acknowledges this problem, as well as the need more generally to expand public as well as private sector services. In 2012, for example, he said:

The real level of urbanization should be measured by the population of registered permanent households, which will ultimately ensure that access to basic public services is fair and equal. This is a long-term process with great potential in which China has vast room to grow…

In China, the service sector currently accounts for 43% of value added and employs 36% of the workforce, whilst spending on healthcare is on average equivalent to 5% of GDP. The potential for development is therefore huge. It must also be noted that China is currently home to 170 million elderly people and has an aging population, so services for older people and health services are industries with huge amounts of employment capacity. In order to fully unlock this enormous potential for development, we therefore need to promote urbanization and the creation of a flourishing service sector in a combined and coherent way, to strengthen policy guidance, and to implement relevant institutional innovations. [2]

China’s general government consumption is around 14% of GDP, while the UK is about 20% (this does not include transfer payments). Health spending in China is around 6% of GDP – in the UK, 9%, Germany and France 11-12%, US (a mainly private) 17%. The 12th 5 Year Plan, which expires this year, highlighted increasing social welfare as a priority.

Back to the UK story – and on to transfer payments. These are part of government spending but not “consumption” in GDP terms. Much of the increase in government spending on transfer payments has been on old age pensions (with people on average living longer) as well as other benefits. A lot of the increase in transfer payments is also because – since the “Golden Age” ended in the late 1970s, and finance capital was unleashed from control, unemployment has on average been much higher. Assuming moreover that a reduction in transfer payments is balanced out by an equivalent reduction in taxes, and that transfer payments on average benefit poorer citizens more, the net effect of reducing them risks benefiting higher income citizens disproportionately.

We also contest John Ross’s argument on the effect of government spending more on public services:

As the government is transferring non-invested private savings into consumption such so called ‘Keynesian’ intervention therefore has the effect of reducing the economy’s investment level – and therefore reducing the economic growth rate.

This is to fall into the classical economists’ error of assuming there is a fixed amount of money which if used for purpose (a) cannot be used for purpose (b). It is a new – and equally wrong – version of the traditional “crowding out” thesis, and also a version of the “banks act as intermediaries” theory.

It is of course fully possible to create new money for investment purposes – government and private consumption and investment are not, from an economic perspective, in competition, if the economy is not working at full capacity. And the least important element – except in politico-ideological terms – is having a modest deficit on the current budget, e.g. to provide, or as an outcome of, a fiscal stimulus.

John Ross’s intemperate attack on those who believe that current budget deficits, at least at any reasonable level, are not a matter for concern, is without foundation. He does not improve his case by political labelling of those who differ from him on this issue as proponents of “academic pro-capitalist economics”!

The aim, surely, is to have a decent society characterised by full employment, with decent pay, low inequality and a fair tax system, providing citizens with good quality key public services – while avoiding high levels of inflation. So long as full employment is not achieved, there is spare capacity in the economy.

The real issue therefore is not whether government runs a current budget deficit, but how a democratic government can achieve its employment and other goals. This indeed means significant and sustained investment, which should be by both public and private sectors – but with the public sector picking up the slack if need be. But it also means spending on decent public services, and providing decent pensions and (as required) benefits. As we all know, benefit spending rises in a crisis or downturn – to which capitalist economies are all too prone.

Deficit spending is a necessary consequence or outcome if government is to avoid depression and disaster. Once the economy recovers and employment rises, government expenditure on benefits falls, tax income rises. The deficit in time evaporates.

But if – as John Ross contends – there must be no borrowing for current expenditure over the cycle, this may mean running gigantic surpluses in the “good years” – presently far beyond what George Osborne so far envisages – to balance out borrowing in the tough times!

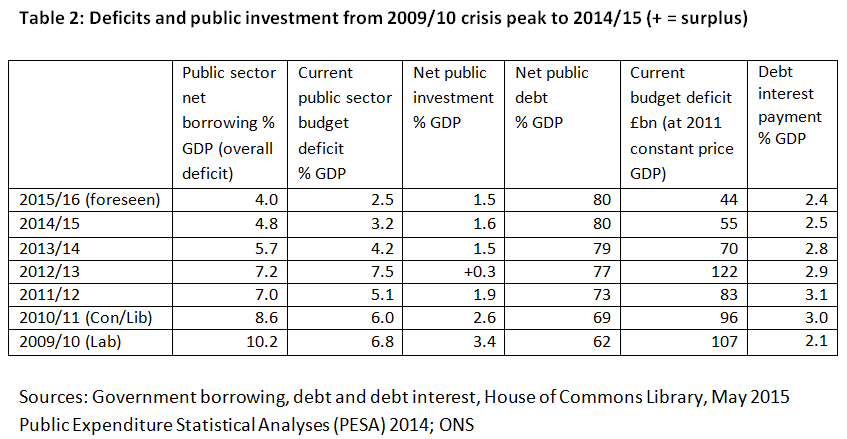

To exemplify the point, this table (taken from a recent post) shows the current and overall UK deficits for the period since 2009/10:

4 responses

Excellent. If you have any connections to McDonnell please make use of them. His advisor Andrew Fisher is surely open to these kind of debates.

Unfortunately, the fact that we are living way beyond our means is illustrated by our trade deficit with the rest of the world. This is approaching 7% of what we call GDP. That imbalance is saving by foreigners and must be exactly balanced by borrowing by us households, the business sector and our government. The reasons for this are manifold. One is the gross overvaluation of our currency (sterling) and another is the gross overpayment of bankers, hedge fund managers, etc who don’t actually make anything of any use. They only raid and deplete our savings just as drones raid and deplete worker bees honey stocks. Bees eventually revolt and evict the drones from the hive.

Yes thanks Danny – but the productive works can be on both investment-related programmes and on "current" activities!

We sure need a counter-meme..

Too sum up, unless we have full employment engaged in productive works, we are not living TO our means.

There’s a counter meme that should be spread.