Over the past decade in advanced western economies, the rate of improvement in prosperity has ground to the lowest point of the post-war period. Stagnation is now the norm across the majority of the globe, and even in Asia more substantial gains are slowing.

This position is illustrated by the comprehensive productivity statistics over time and space on the charts below (for source and details of calculations see endnote [1]).

After a more detailed discussion of outcomes, it is argued in this article that productivity has been the result of aggregate demand rather than supply conditions. And that the strength of demand follows global monetary conditions that are the result of deliberate policy interventions. Prosperity is not a given; it is not a result of natural causes.

The fundamental claim is that the financial globalisation set in motion with the dismantling of the Bretton Woods regime has reversed rather than boosted growth in global prosperity.

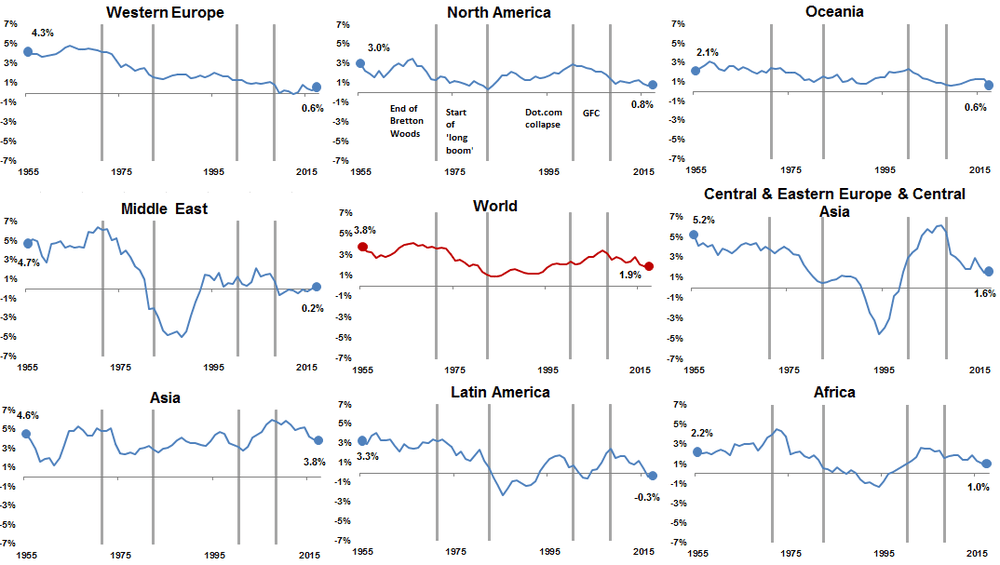

Productivity, % growth

Ten observations

1. Productivity grew with unprecedented vigour in the two decades after the war. This vigour was common to the whole world.

2. The United States (North America) leads a generalised global trajectory, though with a degree of regional variation.

3. The decisive rupture in post-war growth came in 1971 with the dismantling of the Bretton Woods regime.

4. Ahead of the rupture, a steep decline in the growth rate of North American prosperity was already underway (after expansionary excess driven by the Vietnam War and Johnson’s domestic programmes), perhaps motivating the policy change.

5. In the early 1980s global productivity hit an all-time low.

6. The situation was partly reversed through the so-called ‘long boom’, as the Volker shock gave way to expansionary policy.

7. The ‘long-boom’ ends with the new economy / dot.com collapse.

8. Other regions of the world then perform less badly, as prosperity in the West begins seriously to retreat (in part as the West relocated to the East).

9. After the global financial crisis of 2007-08, the stagnation becomes global.

10. Only Asia now records any significant expansion, though growth there is now slowing and has been more remarkable recently than it was in the Bretton Woods era.

Keynes’s theory and post-war policy

Productivity outcomes are wrongly understood as a function of supply conditions; productivity growth was decisively stronger when policy was aimed at demand and there was less emphasis on supply.

An alleged inadequate productivity performance was central to the rejection of the more deliberate management of the global monetary system and domestic economic policy that characterised the early post-war decades. The ‘liberalised’ regime that began as Bretton Woods ended, and that is celebrated as the intellectual victory of von Hayek and Friedman, coincided with a greatly deteriorated economic performance. But while post-war outcomes were regarded at the time as a failure of policy regime, the post-liberalisation outcomes are regarded as a unavoidable fact of nature and pre-liberalisation outcomes now reinterpreted likewise. Crudely characterised, positive pre-liberalisation outcomes were good luck under bad policy; while poor post-liberalisation outcomes were bad luck under good policy.

Inherent to this interpretation is the conventional economic view of a long-run determined by supply and a short run where demand interventions might (depending on your perspective) make a difference (normally – merely – less bad). The long-run is regarded as shown by productivity outcomes: GDP compared with some measure of inputs, most straightforwardly, employment. Paul Krugman’s “productivity may not be everything” signs ‘Keynesians’ up to this doctrine, and even Marxists (repeatedly) see in the trajectory of productivity the inevitable decline in the rate of profit. Keynes however thought no such thing. The General Theory offered the possibility of permanently improved performance in not only the short run but also the long run. “In the long run we are all dead” was a remark from before his major theoretical innovations, and was then redundant.

The purpose of the Bretton Woods Agreement was to permit expansionary policy after the war. Capital control allowed countries to set a low (real) long-term interest rate (‘cheap money’ – see The economic reality is high and rising interest rates ), aimed at both high private investment as well as supporting a greatly expanded role for public expenditure (relative to peacetime norms). The same arrangements were also expected to secure more stable economic conditions.

These policies were underpinned by Keynes’s theory and his fundamental (but little recognised) insight that the combination of orthodox financial policy and orthodox economics caused a generalised underutilisation of resources that also left the system prone to violent instability. Above all this was the result of the monetary authorities allowing a too high long-term rate of interest to prevail (Tily, 2007). The post-war arrangements were aimed at fully utilising all resources through generating permanently higher levels of aggregate demand. They were the means to full employment and a higher standard of living. Cheap money meant higher private investment, and increased government expenditure supported aggregate demand as well as social goals.

It is a grave error of historical interpretation to regard the success of this strategy as a result of chance, or worse only permitted by the reconstruction necessary as a result of total war.

The golden age was the (compromised) result of sustained and profound intellectual and political efforts across much of the globe that had followed the great depression. There was no such success after the First World War: there was only chaos and brutal hardship, punctuated by the briefest excess.

Productivity and demand

But after the Second World War emphasis was gradually shifted to productivity and growth, and prosperity came to be identified with a supply-side agenda, while Keynes’s initiatives were aimed at demand. On the basis of Keynes’s theory, productivity growth is only one dimension of wider policy outcomes.

Any conventional approach to productivity applies only in conditions when there are no idle resources – i.e. full employment (equilibrium or a zero output-gap). With idle resources (i.e. involuntary or under-employment), expanding aggregate demand harnesses those resources.

Given that policy had never before been deliberately operated in this way (except in wartime), and theory had not previously recognised the possibility of equilibrium at a high rate of unemployment, the dynamics of this process were unknown. Moreover, the practice of routinely measuring the macro economy was very much in its infancy, and guidelines for real (as against nominal) measures were not in place until some years later.

We now know that increased aggregate demand led to higher employment and higher production/output, not only higher levels but also triggering robust and sustained economic growth. The measure of labour productivity growth (used above), is simply the ratio of GDP to employment, and reflects the interaction of technology, investment, labour and other market dynamics. World economy productivity grew by 3.5 per cent a year. Crucially, on a Keynes view, (given idle, ill-used or out-dated resources) these interactions are effect not cause. Technology, in particular, is at least in part a function of aggregate demand growth.

The real wage then reflects the extent to which these gains accrue to individual workers, as opposed to the owners of capital. Broadly the labour share is understood as being significantly higher in earlier post-war decades, suggesting workers enjoyed a relatively fair(er) share, and therefore a rising standard of living reasonably in line with productivity.

The global economy better provided for prosperity under Bretton Woods. The mantra today is that globalisation has lifted billions out of poverty, but, on the basis of these productivity figures, the world economy has been bad – or, at best, less good – at generating global prosperity for decades.

From inflation to globalisation

The breakdown in advancing prosperity in the 1970s was not a function of inflation, but a function of abandoning the Bretton Woods regime. Inflation was more consequence than cause of events.

While the economics profession honours the handful of individuals who relentlessly (and most of the time wrongly) warned of inflation probably, from even before the war ended, less emphasis is given to those who wanted to go beyond full employment to ever higher rates of growth (Samuel Brittan, the first FT economics correspondent, issued a manifesto in 1964 under the title The Treasury Under the Tories). And the so-called ‘growthmen’ were immediately more influential – on 17 November 1961 the newly set up OECD agreed a fifty per cent global growth target for the coming decade (quite an initiative for a brand new organisation). The idea that the failure of these stupid and reckless initiatives has any bearing on the validity of Keynes’s theory and policies is laughable.

The vertical Phillips curve that was supposed to prove demand could not be a factor in outcomes beyond the short term has broken down. The curve has been rebranded as a ‘relation’, simply providing a description of conditions not an economic law. Friedman’s relation showed high inflation coinciding with low unemployment in the late 1960s / early 1970s – nothing more.

The termination of Bretton Woods by Nixon, and the parallel liberalisations of domestic credit led to even greater excess – not least the ‘Barber boom under the early 1970s Heath government. Policymakers then clamped down hard. The results of all subsequent policy regimes fell vastly short of those under Bretton Woods. Productivity was greatly weaker on average, but there was also severe volatility – notably the boom of the late 1980s (in the UK, the ‘Lawson boom’), the dot.com excesses, the insanity of the 2000s and finally the global financial crisis.

At this point financial globalisation ended in an event not unlike the Great Depression that was the result of a first globalisation 90 years before. Really it should be no surprise that dismantling the Bretton Woods regime has led to a crisis of the same nature and severity as the one that it was put in place to prevent happening again. And likewise that abandoning Keynes’s theory has brought about conditions equivalent to those that motivated the development of the theory in the same place.

At present the collapse has not motivated any new thinking or changed policy. Still unprecedented levels of global private indebtedness suggest underlying fragilities remain unresolved. Stagnation is the inevitable result of deflationary fiscal policies; quite possibly, only the relentless expansion of central banks’ balance sheets has kept the house of cards from collapsing.

The past teaches us that nothing is inevitable. Yet policymakers who apparently continue to celebrate the wonders of free markets operate as if endless stagnation is now perfectly natural. On the understanding that the great growth of prosperity of the past was not a freak episode but the result of an immensely hard-fought effort to do something about intolerable economic conditions, the case to try and replicate Bretton Woods for today’s world should be irresistible.

Endnote

[1] While the production of economic statistics and associated international standards has been an important advance of economic management and interpretation since the Second World War, long-run historical data even for the biggest economies have always been patchy. But over recent years here have been significant advances in the development of long-run databases with global coverage. The figures here were derived by Rupert Seggins, using the Conference Board’s Total Economy

Database: https://www.conference-board.org/data/economydatabase/

His methodology was to weight together (with GDP) individual country productivity growth figures, taking a five year average of regional and world growth rates for the charts. Productivity is measured as output per person in employment rather than output per hour, because the coverage is better. Conference board adjustments for ICT deflators and for China’s economic size were also used. More detail can be found here: https://www.conference-board.org/data/economydatabase/index.cfm?id=27770

I cannot know the reliability of the Conference Board figures. The aggregates measures for advanced countries correspond to other sources (see this overview here: ‘Productivity: the long global view’, Geoff Tily, ToUChstone blog), and more generally they conform to my prior expectations of outcomes on the basis of Keynes’s analysis.

I am immensely grateful to Rupert for not only sharing his work with me, but also helping to extend his graphical presentation to include the markers for (my) key dates. Note the application and interpretation is all my own.

One Response

Thank you for your article. I would like to ask a question about your conclusion: do you think it will be necessary to replicate the gold-standard part of the Bretton Woods agreement? Another way to ask the same question would be as follows: Bretton Woods was made of two parts, fixed exchange rates and controls on capital movements (plus some additional restrictions that amounted to what some calls ‘financial repression’). Is it possible to separate the contribution of each part to the growth in productivity up to 1971?

My hunch is that capital controls were more important than fixed exchange rates, and their reintroduction would be more of a priority than that of a new gold-standard (which proved untenable anyway).

Thank you,